I believe:

- Valuations Matter

- Nobody Knows

- Structure Beats Activity

This note explains how I think about valuations.

Step 1

I start with ‘structural’ ROIC (Return on Invested Capital) and medium-term growth potential of the company.

- Why Structural: The numbers could be depressed or elevated because of temporary issues in the industry or the business. You must normalize these things. I think in terms of the ability of the business to grow at a certain pace and generate a certain ROIC.

- Why ROIC: ROE is deceptive due to difference in capital structures or cash/goodwill on balance sheet. ROIC is what determines the core profitability of the business.

- Why Medium-Term Growth: Short term growth is factored in the price. Its significantly tougher to establish a confidence band around long term growth. Also, for most value ideas (the ones I look for) as you move out in the future the share of value from those cash flows should be low.

Step 2

I am thinking about the future. Doesn’t it conflict with my second belief: Nobody Knows?

Instead of trying to figure out what the company will do in future precisely, I look at what ROIC and growth is embedded in the price the stock. ROICs typically do not change sharply and permanently. Growth is where there is a wider dispersion in terms of expectations.

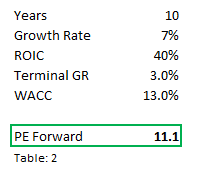

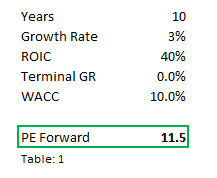

What does a two-wheeler stock trading at 11X forward multiple imply? Table 1 shows the results of a basic DCF model (with some simplifying assumptions). At 40% ROIC you stand to make 10% (WACC) if the growth is just 3% for 10 years and then no growth for ever. Since these numbers are probably lower than inflation this implies volume declines.

What if you want to make 13% on the name? Then the growth should be 7% for 10 years and 3% beyond that. You think of multiple scenariso that give you the current multiple.

Notice in these instances we are not predicting the growth but instead thinking of different scenarios being implied by the current multiple.

.jpg?width=611&height=187&name=1300X300%20Text%20file%20(2).jpg)

Step 3

After establishing the scenarios embedded in the multiples, I start thinking about what the company should deliver on a conservative basis. Given the structure of the market, household penetration, requirements of bottom of pyramid consumer, historical growth rates etc, a 3% growth rate is probably conservative for a two-wheeler company with a dominant franchise in India. But there are other issues to think about – like electrical vehicles taking share or a sudden, sharp, permanent margin contraction. You factor those concerns in the level of margin of safety you want from the name – which is basically buying at a price that makes the embedded assumptions even more conservative.

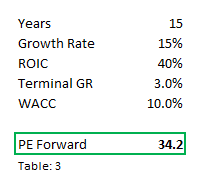

Another example: An IT company trading at 34X one year forward PE is implying it will grow at 15% for 15 years. Terminal growth will be lower for these businesses compared to India focussed businesses as their growth is be linked to global GDP growth. 15% is a high threshold. The way to judge whether this is high or low is not just look at historical growth numbers (which have inorganic component and low base) – but think in terms of structural growth potential. Global GDP growth at single digits, IT spending can be higher by a couple of percentage points and Indian companies might gain some share given cost advantages. Think about these numbers and you will probably arrive at 8% to 10% ‘structural’ growth potential.

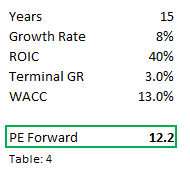

This is the reason why I am happy buying IT companies at low teens multiple. At these multiples even at 8% growth I stand to make 13%. And the chances that the company surprises on the upside are also higher. So, you might end up making more than 13%.

Why not Relative Valuations?

Relative valuations, comparing to peers or stocks own history, assumes history has been correct. Every trade is an assertion that current price is wrong. I am not a relative investor. I cannot sell stock short. It’s easy to ‘rig’ this process.

I do look at these numbers for context. But I want to think in terms of implied expectations.

Pushbacks I often receive:

- Companies are rarely available at such valuations: Yes. That is how it should be. Good ideas are rare.

- You would have missed lot of best performing stocks in the last decade: Probably. But Indexes have broadly delivered 12% to 13% over long periods of time which in turn is determined by earnings growth (very similar) based on India’s nominal GDP growth and formalization. If you can find few ideas occasionally, that can do better than this – you should be fine. FOMO (fear of missing out) is a source of most investing mistakes. I will miss a lot of businesses that do well. I will be fine. Type two errors are acceptable to me.

- This is too academic. Market doesn’t think this way: That’s precisely the source of any alpha this approach might generate. What ‘market’ thinks can often make outcomes noisy in the short term. But over medium-term business prevails. First principles prevail. Investing fundamentals prevail.

- There are lot examples where this fails: Of course, there are. This approach (or any other sound approach) just tilts the odds in your favour. It helps create a portfolio that is exposed to serendipity – to the possibility of more good things happening to you than bad.

You will never be able to buy deep cyclicals: Not true. There is a price at which even a 5% ROIC company might be a good investment. The risks of accidents in these ideas are high. You must incorporate the risks in higher margin of safety that you demand in such cases

The funds I manage are expressions of the principles outlined in this note.

Leave a comment