-3.jpg)

Dear Investor,

With stock indices near record highs, it's likely that your equity portfolio has grown substantially. Some of you may be regretting not having invested more. Others may be anxious due to the sharp rise and wondering if they should be reducing exposure.

Today having access to information can also make investing more challenging because there's so much noise to filter through. I don’t envy your position navigating different opinions coming from blogs, podcasts, interviews, reports, etc. - some of which might even be conflicting. However, you possess an overwhelming advantage in the simplicity of the plan you need to execute:

- Save consistently.

- Maintain the right asset allocation.

- Be patient.

All the good advice you receive tries to reinforce these boring and useful principles. Your Savings protects you from ups and downs in markets and in life. It helps you avoid hasty decisions when you're worried. It gives you the freedom to make personal choices that are aligned with your values and free from financial constraints.

SIPs, or Systematic Investment Plans, are a practical way to save regularly. With SIPs, you invest a set amount each month.

Maintaining the right asset allocation is key to staying invested. For many investors, the return on their total investable net worth is often in single digits. This is due to pro-cyclical behaviour (chasing performance). If you have higher allocation to equities, compared to your risk appetite, you might be tempted to sell during sharp market downturns - which can be the worst time to do so. Conversely, if you are too conservative, you might end up increasing risk in your portfolios just as the market peaks, driven by frustration with your returns.

The right asset allocation helps you stay invested for the long term and avoid poor decisions at market extremes. If you are unsure about the right asset allocation for you, you can seek the help of a good advisor.

Maintaining a diversified portfolio also means acknowledging the uncertainty of the future. Even in a country as capitalist and innovative as the United States, markets stagnated for 16, 19, and 25 years at a time in the last century1.

I would strive for satisfactory returns in different market conditions – good or challenging – rather than targeting the highest returns only in the best situations.

Today, if unsure between two investment choices – I would pick the one that is more conservative.

In the appendix, I share some views on markets and the portfolio I'm managing for you.

Thank you for staying invested.

Regards,

Abhishek Singh.

Appendix (Exciting & Not So Useful)

Views On Markets

- I don’t know what markets will do in 2024.

- I would temper return expectations for the medium term. For most investors, Equities should be at the core of their portfolios. But please note that the returns are not linear but lumpy.

-

Markets are expensive. I thought this was the case a few months earlier as well. You can always find some bottom-up ideas, but Financials are probably, in my opinion, the only sizable sector where valuations seem comfortable.

The Good

I try and run similar portfolios across both the DSP Top 100 Equity Fund and DSP Equity Savings Fund.

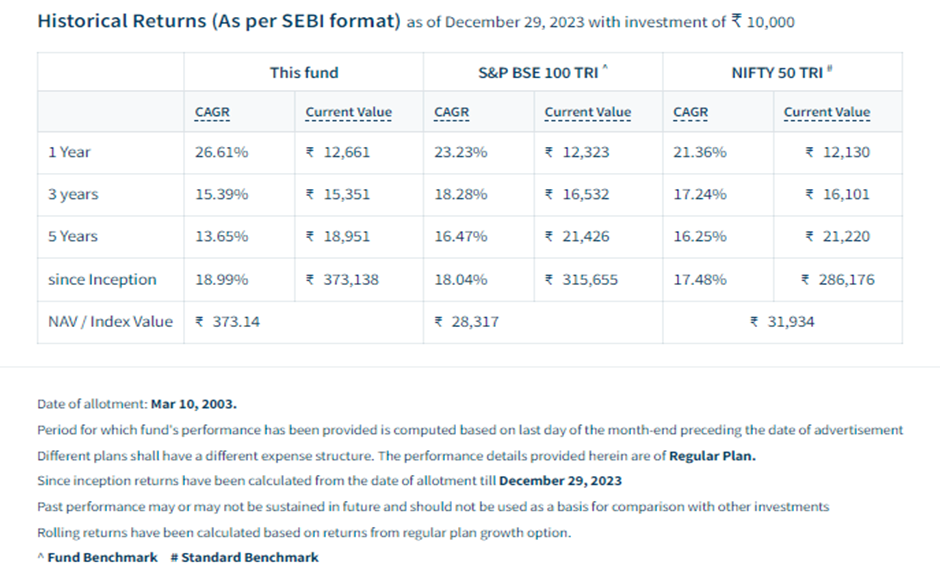

DSP Top 100 Equity Fund (Regular Plan Growth Option) delivered about 26.61% return as of December 29, 2023. This was 3.3% higher than the benchmark. One year performance is noise in Equity. In future letters, we will not discuss performance until we reach the 5-year mark. In Large Caps Funds, 80% of the exposure must be to Large Caps (AMFI definition) only. At this point, I believe Large Caps are better placed compared to Mid/Small Caps.

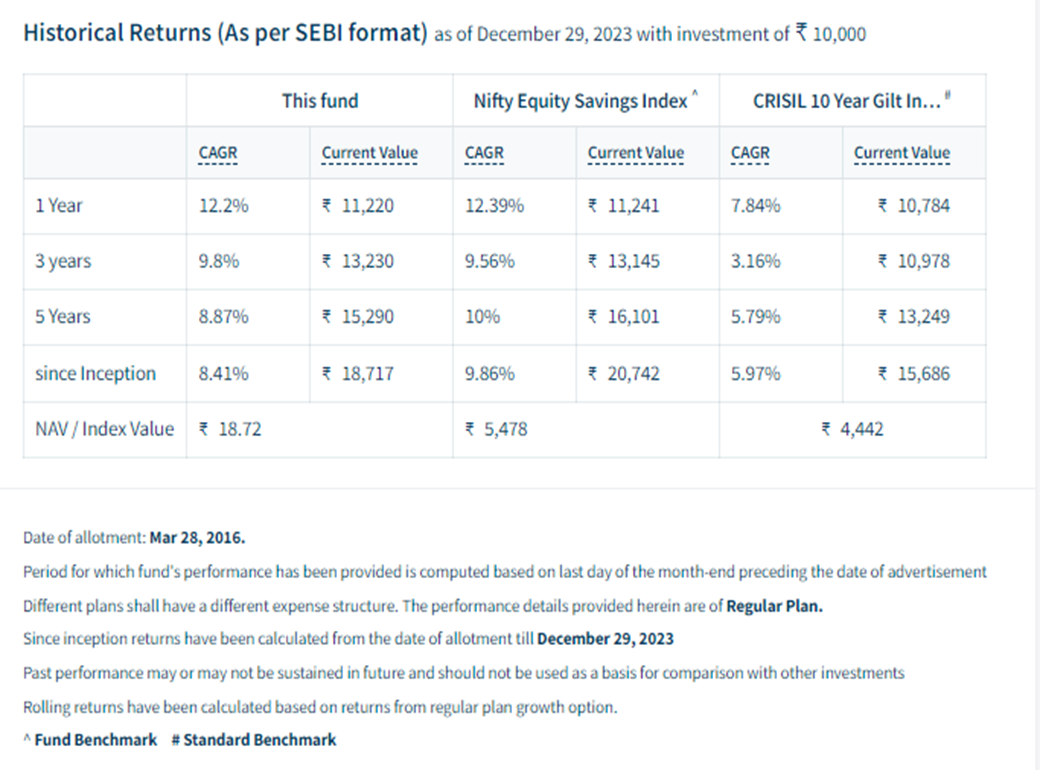

DSP Equity Savings Fund (Regular Plan Growth Option) delivered a 12.2% return as of December 29, 2023, which was 20 bps lower than the benchmark. However, there are multiple nuances when you compare hybrid fund performance to benchmarks. The category itself is not homogenous. Different funds are trying to address different needs. We will focus on absolute returns here. In the DSP Equity Savings Fund (35% to 40% Equity which is hedged with Index options, about 30% Arbitrage which leads to Equity taxation, and the rest broadly in fixed income securities) we continue to incur the cost of hedges. In case of a large correction, when and if it happens, we expect to recover these costs. 75% of the Equity portfolio is invested in Large Caps today. I intend to keep it a Large Cap biased portfolio. The fixed income part of the portfolio is run akin to a high-quality short-term fund with a duration range of 2-3 years.

The core of most ideas that worked for us (Pharma, Tata Motors, ONGC, etc) was that implied expectations (for profitability/growth) at the point we bought those stocks - were too conservative. In some cases, the negative value was assigned to some parts of the business. And the interesting thing is in many instances even the management/promoters were not positive on the near-term prospects of the business. But markets have a habit of surprising the consensus. We will try and buy ideas where the story is bad but not as bad as the price is building in. This, in my opinion, is the only intelligent way to operate in a world that consistently surprises the consensus.

Even in a market, which for a valuation-conscious investor is challenging we have been able to stay close to our framework. Today there is only about 15% - 20% odd weight where I feel the assumptions are getting stretched.

The Not So Good

There were at least two instances where I probably made avoidable errors in analysis. Where I had all the data needed but I made mistakes in establishing the correct valuation band for the businesses. Every year there would be some such instances. We learn from them and improve our toolkit.

There were situations where I felt there was an opportunity (Asset Management space for example) but before I could make up my mind the stocks rallied beyond my comfort band. It’s a continuous and tormenting process.

Lastly with the benefit of hindsight being conservative might seem like a mistake. Any aggression – whether in terms of higher overall equity exposure, or higher exposure to Small/Mid Caps vs. Large Cap has been rewarded. I am not sure this was a mistake.

This highlights one of the core challenges of my profession – it’s not easy to judge whether a decision was good or bad even after the event.

The Usual

Apart from valuations another challenge has been a narrative-driven market. For example, some large Infrastructure businesses will probably end up delivering single-digit core profit growth from Pre-Covid to FY 2025. This is assuming higher normalized margins by then. And the best-case ROE (Return on Equity) they will generate is probably in mid to high teens. Investors are thinking of them as an India Infra proxy while a large part of the order book has been driven by the middle east where there have been significant write-offs in the past. The share of the public sector in the order book is significantly higher than in the 2007 cycle. This puts pressure on margins. Markets have still rerated them from teens earnings multiple to more than 30x PE2.

Today one of the best banks in India is getting a lower Price to Book multiple than a transmission utility.

In a data, noise rich, and volatile world, we will try and stay close to first principles.

The portfolio is skewed towards Financials (Banks, Life & General Insurance, NBFCs), Pharma (India, US Generics, CDMO), and Autos (Global, India 2W, India PV).

If markets are broadly expensive, should I be more diversified? I believe it’s my responsibility to take these active calls on your behalf and tilt the portfolio towards wherever I find the risk-return most favourable.

Any outperformance compared to the benchmarks, over the longer term, will be a function of how different the portfolio was (from the benchmark) and how right I was about these differences.

All my personal, incremental Equity allocation goes to the DSP Top 100 Equity Fund, and all ‘Debt’ allocation goes to the DSP Equity Savings Fund. The latter carries a higher risk than fixed-income schemes but over the full cycle, I expect it to do reasonably well – especially on a post-tax basis.

For any queries related to the portfolio of the funds you can write to:

At times, fund managers are accused of trying to sound intelligent by offering conservative views as bearish arguments sound clever. On the other hand, it is optimism that works in equity markets. Equities have delivered reasonably high real returns over decades.

This optimism should reflect in your asset allocation, in your exposures, to the extent your risk appetite allows. But do you want the person – managing this exposure – to rather err on the side of gullibility or skepticism? Something to think about.

Let me reiterate that it’s a long journey. We aren’t in a hurry.

Hope you have a great 2024.

DSP TOP 100 Equity Fund - Performance of Regular Plan Growth Option

DSP Equity Savings Fund – Performance of Regular Plan Growth Option

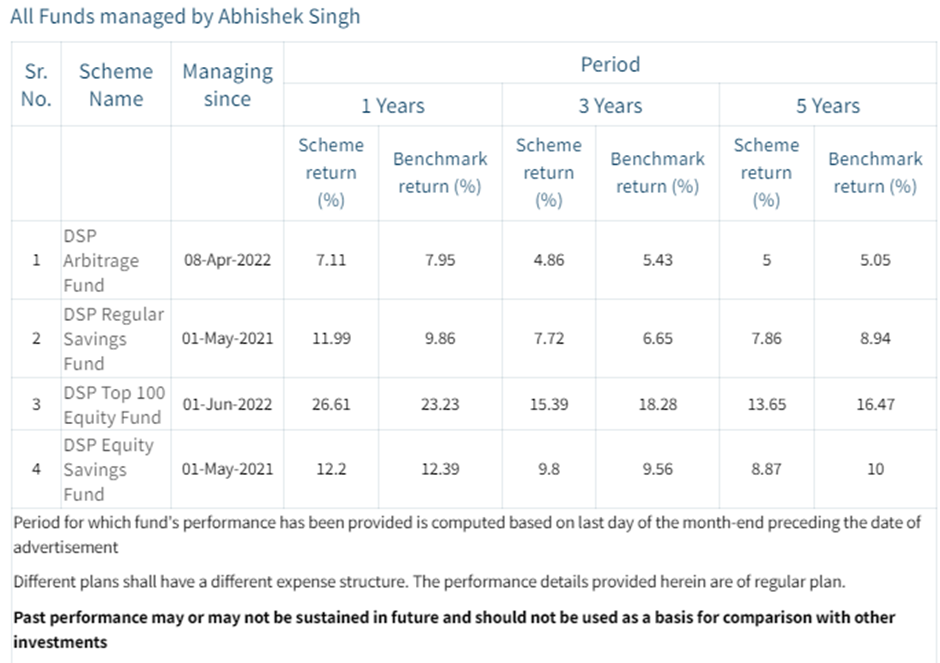

Performance of other schemes managed by same fund manager

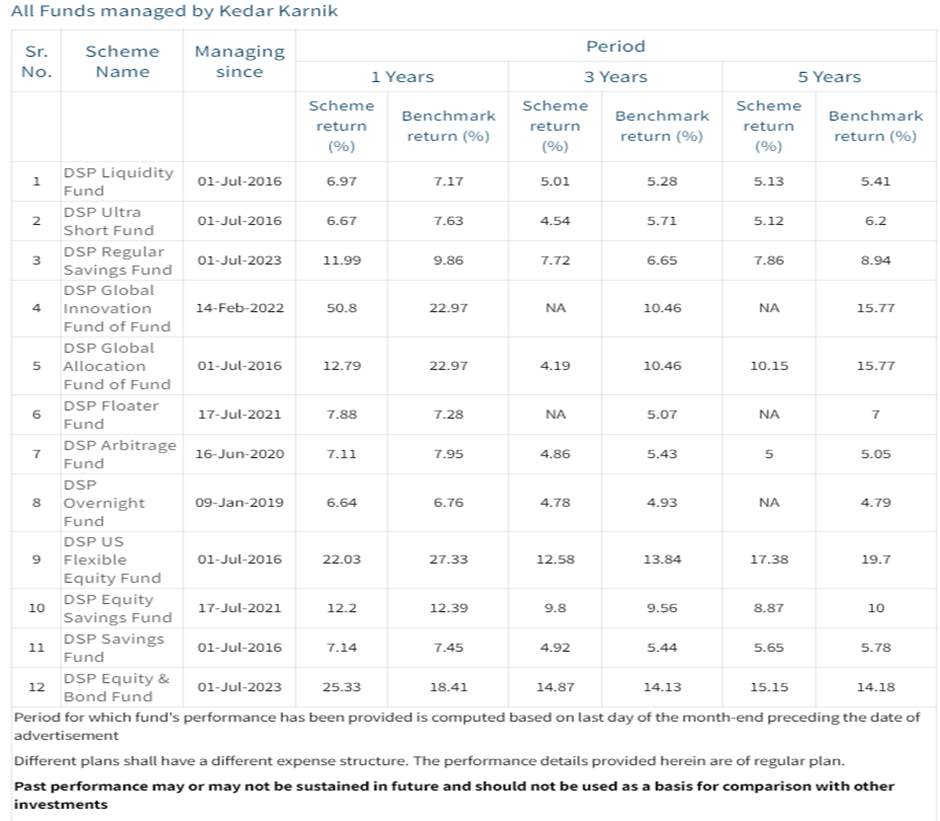

Performance of other schemes managed by same fund manager

.png?width=1764&height=1242&name=image%20(15).png) *Investors should consult their financial advisers if in doubt about whether the Scheme is suitable for them.

*Investors should consult their financial advisers if in doubt about whether the Scheme is suitable for them.

1Source: (https://www.marketwatch.com/story/the-dows-tumultuous-120-year-history-in-one-chart-2017-03-23).

2Source: Bloomberg

Leave a comment