February 2023 edition of Netra is out. Netra is DSP's one of a kind in-house research-based product that extracts and presents market insights ahead of time. Click the link below to check out all the available editions.Go to Netra

With a global economic slowdown and rising inflation, there has been significant impact on the world economy.

Let us dive into the latest happenings in the global markets and how they have impacted individuals, corporates, and Governments.

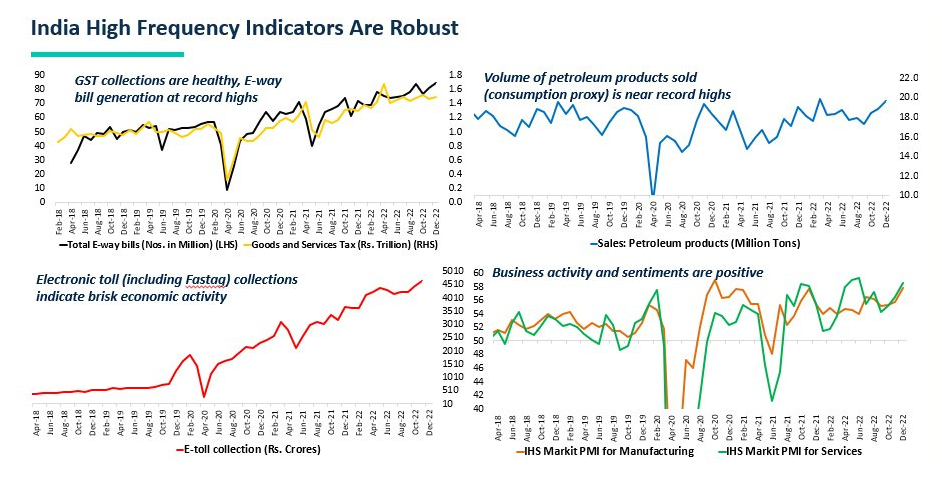

India’s high-frequency indicators show steady economic growth

Source: CMIE, DSP As on Jan 2023

India’s economic growth has remained stable despite a shift towards economic slowdown worldwide. Looking at the tax collections, GST is bringing in a healthy inflow. In December 2022, the GST collection was approximately Rs. 1.5 trillion. However, the GST collection for 2022 peaked in February, with a record collection of slightly over the Rs.1.6 trillion mark. Moreover, the E-way bills introduced under the GST regime are being generated at a record high rate. December 2022 saw the generation of over 80 million E-way bills, the highest it has ever been. Electronic toll collections, including Fastag, have also soared over the year. This indicates brisk economic activity as it recovers in the post-pandemic period.

The volume of petroleum products sold is also close to record highs. December 2022 witnessed almost 20 million tonnes in petroleum sales, a steady increase from August 2022. Assessing the parameters, we can conclude that business sentiments and activities remain positive, indicating growth potential.

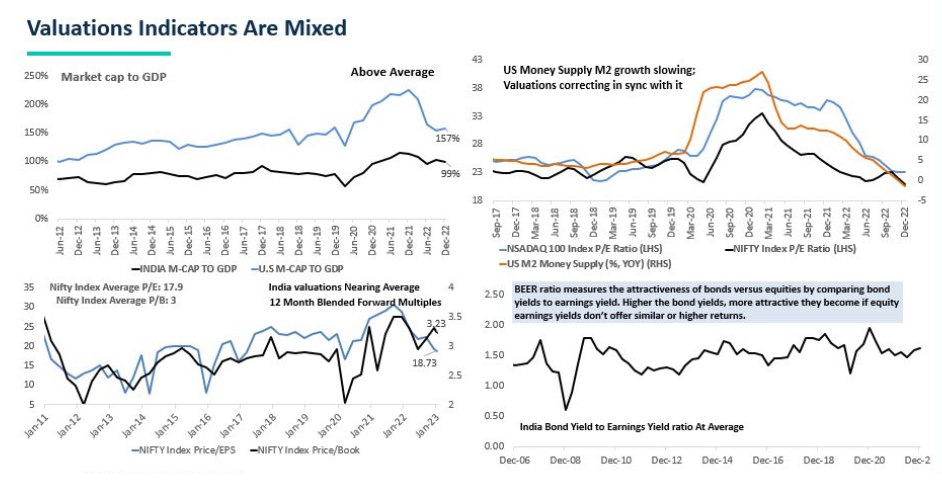

Value indicators show mixed results

Source: Bloomberg As On Jan 2023

Value indicators have displayed mixed results, with some showing above-average performance and some returning to the historical averages. The US market cap to GDP was 157%. This was fairly above the Indian market cap to GDP indicator, which was at 99%.

If we look at the US money supply M2, growth slowed. Subsequently, the valuations were corrected in sync with it.

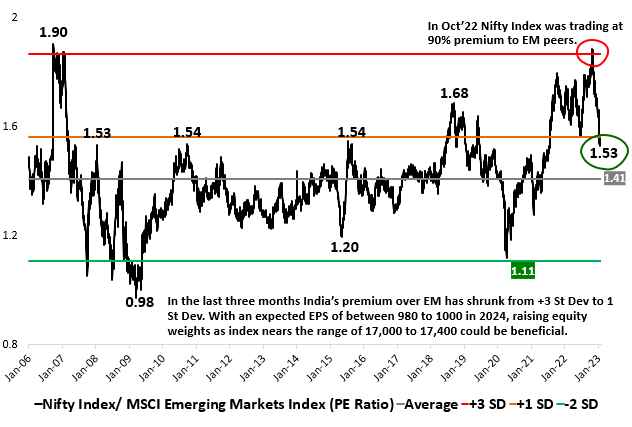

India’s premium over EMs withers away

Source: Bloomberg Data as on Jan 2023

There is good news for Indian equities. The premium that Indian equities enjoyed over the Emerging Market (EM) peers has vanished. Previously, India’s shining EM equity performance was not linked to India outperforming other markets. Instead, it was the underperformance of other markets that gave India this premium.

However, if we look at the previous three months, Nifty has been flat, as opposed to a rallying performance of the MSCI Emerging Market Index. This correction has led to lower FPI flows as the valuations have increased.

Overall, this has been a positive shift for Indian equities. It is expected that in 2023, if there is further consolidation and steady growth in earnings, India can once again become an attractive market.

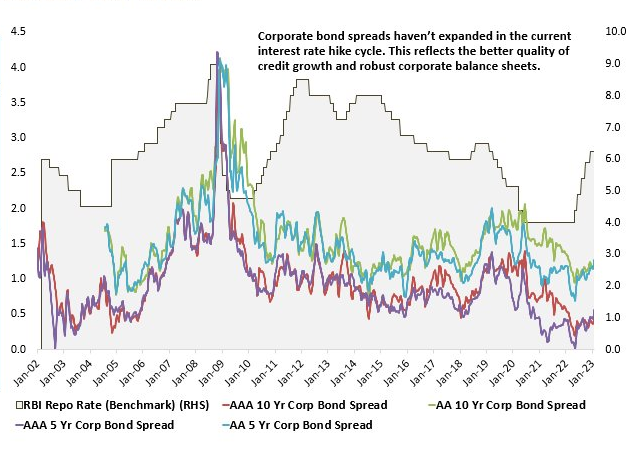

Corporate bond yield spreads show trend-defying results

Source: Bloomberg Data as on Jan 2023

Bond yield spreads are calculated by deducting the Government bond yield from the corporate bond yield for a ten-year period. This is because corporate bonds in India give a premium over their Government counterparts.

Over the years, the trend has been that a spike in corporate bond spreads is seen every time the interest rates are hiked. This indicates that the balance sheets are weak, and when they coincide with tight financial conditions, there is a sharp increase in the spread.

Over the last 9 months, the RBI has raised the repo rate by 225 basis points. This, typically, should have shown a substantial increase in the corporate bond spread. However, the spread has not expanded in this cycle of interest rate hikes, making it the least restrictive and disrupting cycle for corporate bonds. In fact, the AAA corporate bond spread is almost 40 bps lower than the long-term average. This is a reflection of strong balance sheets and better credit growth.

All of this can prove to be extremely beneficial for the corporates in India, which will be in a position to borrow at lower interest rates.

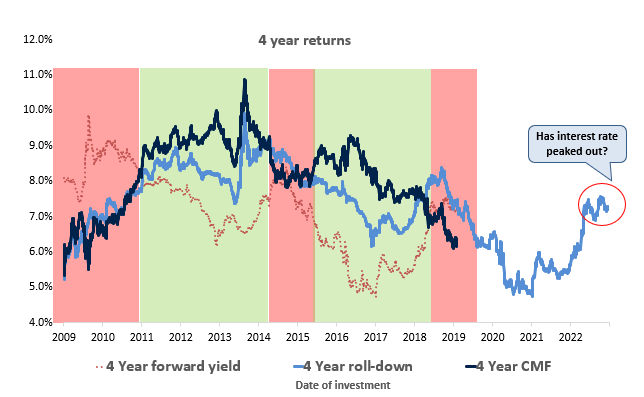

A preference builds for CMFs over Roll-down funds

Source: Internal, Bloomberg, DSP As on Jan 2023. Returns of 4 year constant maturity fund is calculated assuming monthly rebalancing

Constant Maturity Funds (CMFs) keep a constant duration by buying and selling bonds periodically. On the other hand, roll-down funds start with a higher duration, which keeps declining till the time the fund reaches its maturity.

The peaking interest rates have created a better environment for picking actively managed CMFs. Here’s why. As interest rates rise, CMFs tend to fetch better returns than roll-down funds. This is because a longer duration in CMFs allows investors to earn better marked-to-market gains. At present, the rates seem to have peaked or are about to. This point in the cycle is an excellent time to consider constant maturity debt funds.

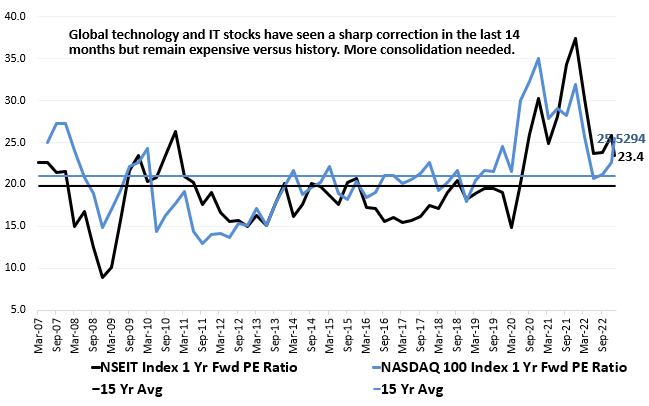

There is a correction in technology stocks

Source: Bloomberg, DSP As on Jan 2023

During the previous 14 months, IT stocks have seen some sharp corrections. The Nasdaq 100 Index fell 28% from its latest peak, and the Nifty IT Index, too, saw a decline of 22%. If we look at Nasdaq, the one-year forward price to earning multiple is down to 25 from its peak at 35. As for Nifty IT, the multiple has reached 23 from its high of 37.

However, technology stocks are still correcting and are not cheap enough yet. There is still room for further consolidation as the advanced economies are on the brink of an economic slowdown. If you are an investor waiting to jump in and buy into this price correction, you are likely to get a good opportunity to do so.

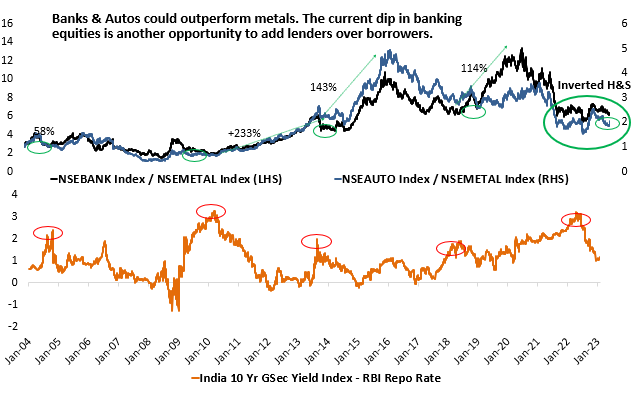

An opportunity to own banks and autos over metals is rising

Source: Bloomberg Data as on Jan 2023

When the economy is stable and prices of commodities normalise, those who borrow and use commodities tend to do better than those who sell them. The ratio of lenders to borrowers is established by looking at the ratio of the NSE Bank Index to the NSE Metal Index. At present, this ratio is at a multi-year low. This came at a time when the yield curve was steep, and the RBI was about to hike the rates.

Since this phase, banks and autos have been seen to be top performers, while metals have gone down. A similar favourable condition has been observed during a recent correction in the banking stocks and a rise in metal equities.

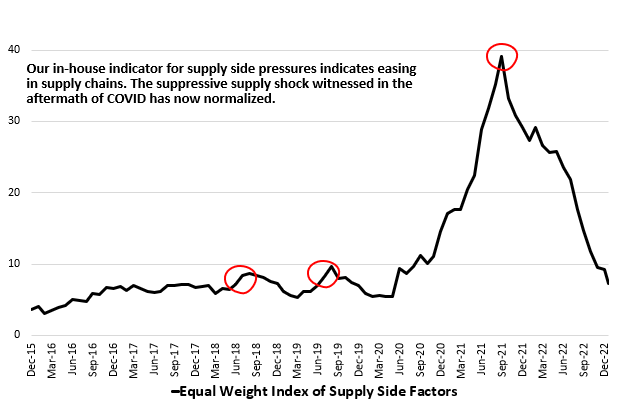

Supply chains are normalising

Source: Bloomberg, DSP As on Jan 2023

Supply-side pressures have reduced in many markets, especially the ones that had disrupted supply chains during the whole of 2022. The indicator for world container freight rates, shipping freights, and the backlog of orders has eased. This can reflect positively on the rising inflation levels by giving more space to central banks to pause the constant hikes in interest rates.

The situation in the US

There has been an economic slowdown in the US, which has led to reduced profitability and contracting growth for the corporates. Consequently, the stock market has seen a long correction and consolidation phase. Moreover, after the interest rate hikes by the Fed in the last 9 months, economic growth is likely to slow down further.

For some time, US equities will keep consolidating, and valuations are going to witness more corrections. However, this can be a good time for investors to build their equity positions through systematic investment plans (SIPs).

The UIG, or the underlying inflation gauge, is used to provide a measure of the underlying inflation. It has outperformed core inflation measures to give more accurate forecasts over time. The latest data predicts that the UIG is set to decline rapidly. Because the CPI inflation follows UIG very closely, it is predicted that the consumer price index in the US is set to go lower than the 5% reading in the upcoming few months.

At this point, the Fed faces another test. Interest rate hikes now can worsen the situation, which is why the Fed is likely to abstain from them hereon.

The bottom line: Unlocking India’s potential

In the present scenario, India has among the best growth potentials in the world. We are moving in the right direction, but what we need is the pace to catch up to the current leaders.

India has the second-largest urban population, just below China. This opens the potential for large consumption by urban dwellers. However, India is still far away from catching up with China. If we look at the installed thermal and nuclear power capacity, metro-enabled transportation, and capacity of the ports, there is a stark difference between the two countries.

While we have the potential, we now have to see how we can pace up our efforts to reach the required level of growth.

Leave a comment