The title of this blog post might lead you to believe that we are here to discuss the philosophy of life. However, just assume for a second, that you are a hedge fund manager, and that the stock market is in a free fall. And now read the title again. Isn’t this a refreshing perspective?!

Most investors in the market only see one side of it. The long side. The buy-and-hold side. The side where investment gurus stealthily drop ‘stock tips’ accompanied by steep target prices. No doubt that this side of the market is one where substantial wealth can be created. But it is not the only side. There is a ‘short’ side to the market as well. One that requires not just a different skillset, but also solid risk management. If done well, however, it can be not just complementary to the existing portfolio, but also profitable. This is not about just going outright short or outright long, but trying to balance these well. This post touches upon my experiences as a hedge fund manager in India and the uniqueness of this market. I hope it will help you appreciate this interesting world, and the possibilities for you as an investor.

A Greek and Nordic history

“Short sellers are the market’s police officers. If short selling were to go away, the market would levitate even more than it currently does.” - Seth Klarman

I started my career with an American Investment bank in London and worked in their internal proprietary investment team. One of the first things I was told when I joined was, “An asset does not know it can only go up!” This set the tone for the next several years of intensive investment training. It involved employing a variety of strategies – long short equities, capital structure arbitrage, merger arbitrage, macro, convertibles, mezzanine and distressed debt. Was there a common thread? Yes, the need to remain balanced.

Drawn by the volatility and dispersion which existed in India, I came back a decade ago to implement the basics of hedge fund investing I had been armed with. However, the starry outlook was jarred in my first few meetings here itself – “You cannot short in India – it does not work!”

“Did I catch the wrong flight?”, I wondered. Thankfully, some stubbornness and an inherent self-belief pushed me to stay the course.

I looked back at the time, at how I had invested in both Nordic and Greek equity markets with equal success. These were assets which were very different in nature – fundamentally, culturally and behaviourally. What had aided me was always sticking to first principles – that operating fundamentals combined with risk management is what matters in the end. Hence I was determined to trust my training and adapt to a new market, yet again. In retrospect, the last decade has been an interesting journey and a great learning experience.

What really matters

Many things matter for a stock’s performance, and there are a number of factors simultaneously at play. However, my view, is that in the end, it is the business cycle which matters the most. Let us take a look at some sectors below, which went through some challenging times. We’ve taken sector earnings ratings changes as a proxy for such cycles, and the associated stock price changes.

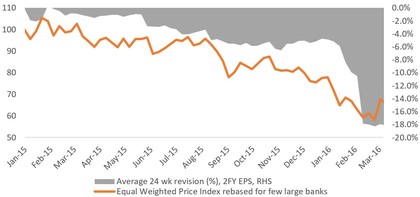

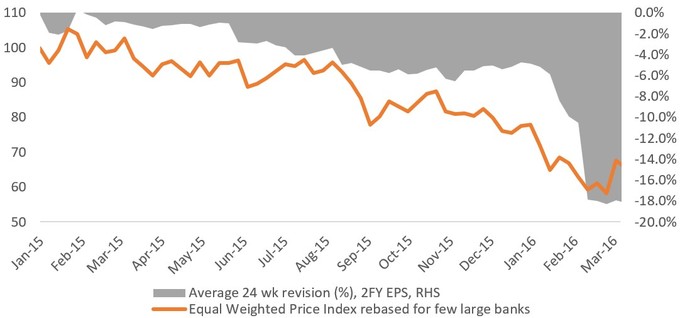

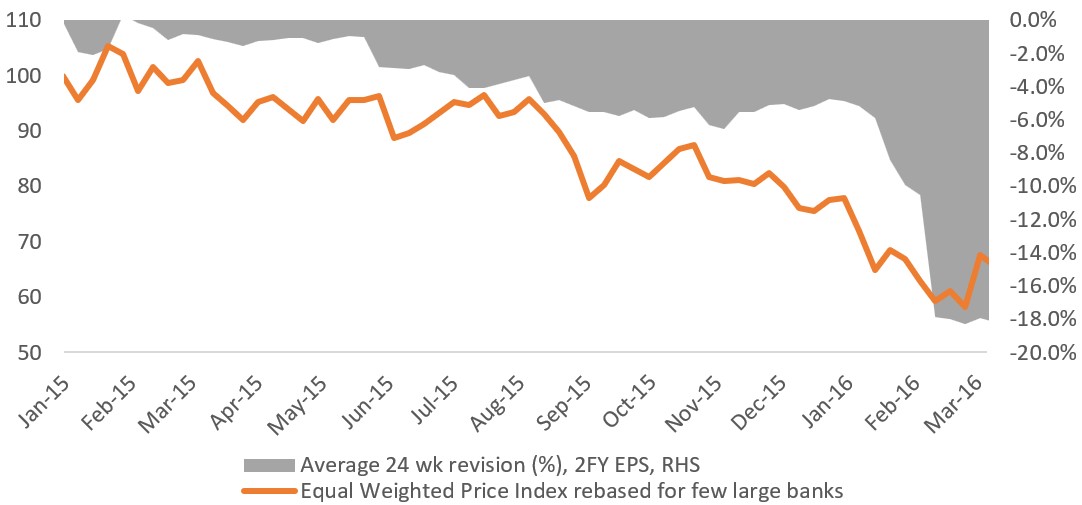

1. The corporate bank asset quality down-cycle in 2015/16. This was right after the Reserve Bank of India directed banks to dig deep and clean up their books. Unsurprisingly, earnings were downgraded sharply, which also caused share prices to follow suit. Below is a chart showing the earnings downgrades and price moves of 3 large banks during the time. As you can see, when the fundamentals weaken, price moves accompany. Hence looking to always be long an asset will not generate returns during such periods.

Note: We have used average 24-week earnings revisions because in the short term, there is volatility and the trend does not get captured clearly while using point to point estimates across multiple companies.

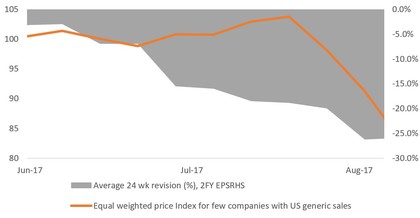

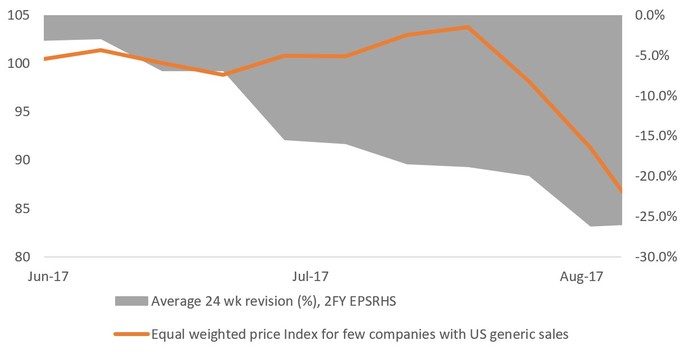

2. Next below is the pharma sector. In 2017, the regulator USFDA (US Food & Drug Administration) came down heavily on plant and process quality of pharma companies in India. Several plants were hit with ‘import alerts’, meaning they couldn’t export any products to the US until the problems pointed out by the USFDA were fixed. Earnings downgrades followed, as did stock corrections. Today, many years later, there are some plants that have still not received clearances. Do note the downward earnings revisions and associated price weakness

Source: Elara Research, Stocks/ sectors mentioned in this note do not constitute any research report/recommendation of the same and the Representative Portfolio may or may not have any future position. Past performance is not a reliable indicator of future results.

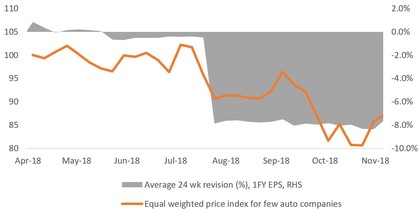

3. You would remember the ILFS (a large NBFC) crisis from 2018? Liquidity dried up, which impacted the availability of vehicle financing and this led to downgrades in the 2-wheeler space. Once again, stock prices corrected, and the business cycle had quickly turned.

Source: Elara Research, Stocks/ sectors mentioned in this note do not constitute any research report/recommendation of the same and the Representative Portfolio may or may not have any future position. Past performance is not a reliable indicator of future results.

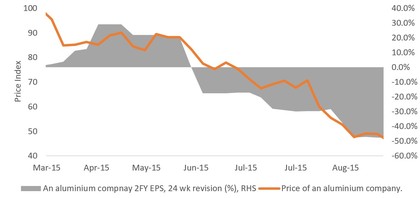

4. Our last case study would be Metals from 2015/16, and we can take Aluminium as an example. One of the largest producers was barely breaking even with a cost of production of USD 1700, while the LME price was USD 1800. The Street had lofty expectations, but our view was that China overheating would lead to earnings downgrades. This is how it played out.

Source: Elara Research, Stocks/ sectors mentioned in this note do not constitute any research report/recommendation of the same and the Representative Portfolio may or may not have any future position. Past performance is not a reliable indicator of future results.

In my view, such cycles tend to play out time and again, irrespective of short term market moves. It is our job to identify such trends. But technical capability aside, one critical requirement for successfully managing a hedge fund is equanimity. I have had to take positions in ideas where I would have to flip from being short to being long on the same stock or vice versa (such as in the Aluminium example above) because the underlying data changed. Hence, objectivity is paramount. Being emotionally attached to a one-sided view could be crippling otherwise. This is easier said than done, of course, but we try to maintain discipline – of following the data rather than the narratives.

The Short Road

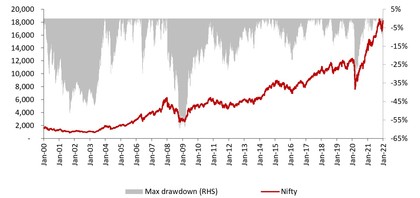

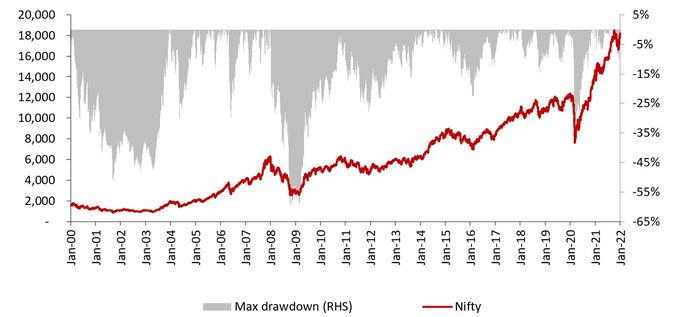

But the path to shorting-greatness is stacked against investors. Take the case of a bull market like we are in now. Over the last year, the Nifty 50 hit an all-time high not just once or twice, but 48 times! Further, there was a streak of 197 days in 2021 where the market didn’t correct more than 5%. These might be rare occurrences during a larger time frame, and a look at the 20-year Nifty chart confirms this. Drawdowns can be sharp and material, and when they do come, it is good to have the flexibility to go short.

Source: Ambit Research, Past performance is not a reliable indicator of future results

Some think shorting is all about technicals and charts. It could be, but my investing style is purely fundamental bottoms-up. What do I look for in short ideas? Typically, one or more of the following: weak industry structure, no competitive advantages in the industry, poor management quality, well-below market expectations on 9-12 months’ earnings power, poor free cash flows, material overvaluations, and unfavourable economic drivers, to name a few.

Here are some important aspects that make shorting quite challenging, if not done prudently:

1. The ecosystem is inherently bullish. This is the same story globally but slightly more so in India.

- Companies and management are prone to giving out bullish commentary and outlook.

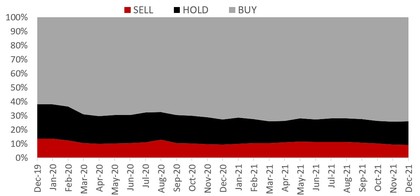

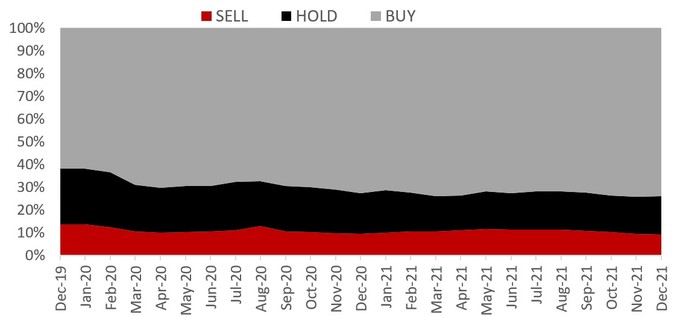

- Sell-side research too tend to have a bullish bias in their reports. Only ~10% Sell recommendations compared to ~90% Buy and Hold. Have a look at the median buy/sell/hold recommendations across the top 100 stocks over the last few years in the chart below:

Source: Ambit Research.

2. There are multiple technical nuances stacked up against shorting.

- Much capital goes to back long investments. In our experience, at least 95%+ (conservatively) of the AUM chasing Indian investments are all on the long side.

- The sizing of a short position goes against you when you are wrong. Think of it this way. If your long position goes down by 50%, then your problem halves. i.e. if you like a long idea and make it 10% of your portfolio, it now goes down to 5%. However, when your short position goes wrong by 50% - your problem magnifies, i.e. if you took a 10% short position, it now becomes 15%. This makes it difficult to average down in a short.

- There is also an unlimited downside (theoretically) on a short. On a long bet, you can only lose 100%. In a short gone wrong, however, the loss can be multiples of the capital invested. If you short a stock with no business to speak of, at USD 20, and expect the stock to go down to zero, that could be a good trade. But imagine if this stock rallies to USD 325 just a handful of trading sessions later. Sounds ridiculous, but these are actual share price numbers of an American video game retailer from just a year ago!

3. There are some India-specific nuances to keep in mind as well:

- In global markets, shorts are typically arranged through prime brokers, utilising a Stock Lending and Borrowing (SLB) mechanism. The borrowing of the stock adds an interest cost layer as well to the short seller. In India, this SLB market is less liquid, and participants, hence, prefer the single-stock futures market instead for shorting. This is less complex to execute, perhaps, but also limited by the number of F&O (Futures & Options) instruments available – which is regulated by SEBI (the regulator).

- Position sizes too are restricted by specific limits imposed by the Exchange. These are called MWPL or Market Wide Position Limits. To put it simply, every stock has certain restrictions placed on it, based on parameters determined by the Exchange. These restrictions include how many shares/contracts can be traded, which instruments can be used, how much leverage is allowed, which participants can hold what (like how much can be held by mutual funds, foreigners, individuals) etc. The MWPL is set at 95%, which means the aggregate open interest cannot be more than this number. Crossing this threshold results in the stock being placed in a ‘ban’ list, which in turn means new positions cannot be taken, existing positions must be squared off, settlement at expiry would need to be physical and so on. The Exchange monitors all this so that market manipulation is reduced, which is fair. But this does also limit the available shorting opportunities from time to time.

- When a stock goes into a ‘ban’ list due to high volatility or due to too much capital chasing a short idea, one is never able to capture the full benefit. Ironically, this happens exactly when a short thesis is playing out.

- F&O positions exist in a limited number of stocks (~197 as of the time of this writing). The number has grown recently, but does not capture the whole universe available to go long. This selection typically has a positive bias – i.e. high quality companies keep entering while lower-quality ones keep exiting when they fail to meet required criteria. Hence you can rarely hold a short to zero!

All of these technical nuances mean that shorting is a specific skill set which is quite rare. Especially when the market goes one way up like over the last couple of years, outright short positions undergo pain. However, during periods of mean reversion (whether at a stock or market level), shorts help by:

1. Capturing dispersion in a sector. It’s not just a long position in the stock going up that generates returns, but a short position in a stock going down can generate returns as well.

2. Providing downside protection, lower volatility, and limiting drawdowns.

"Success is relative"

Investors do not always have to be either outright long or outright short. There is an opportunity set called ‘Relative Value’, which refers to an idea encompassing both, i.e., a long component, and a short component. This could be market neutral, sector neutral, factor neutral, and so on. As an example, given the potential for strong growth in India’s aviation sector (some estimates suggest nearly 1 billion people have never flown before), it may not be prudent to short an airline stock outright. However, it might be worthwhile going long one airline stock while going short the other, pocketing the relative spread between both positions, irrespective of how the overall sector itself moves.

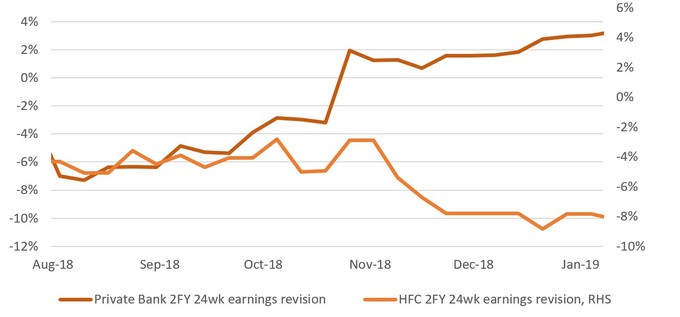

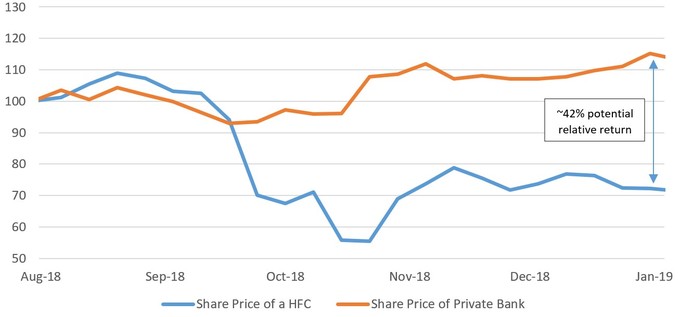

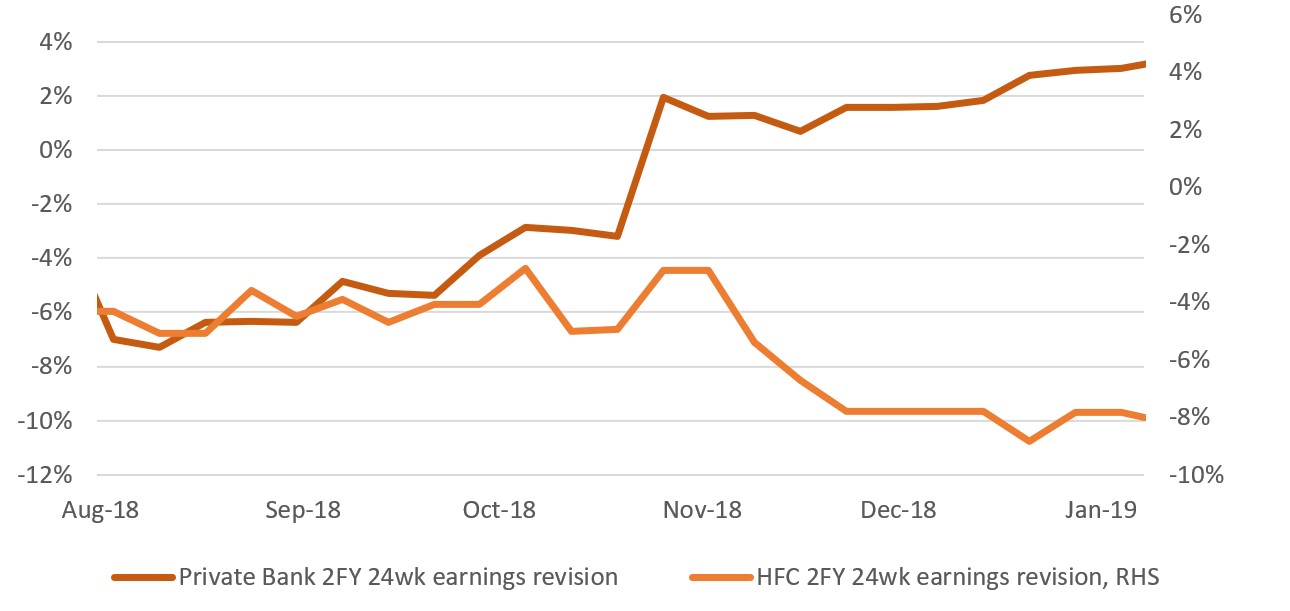

Here below is one such example, pitting a private bank against a housing finance company (HFC). Credit growth for the bank was expected to pick up, while disbursements at the HFC were taking a knock in addition to credit quality issues. This led to earnings upgrades for the former, and downgrades in the latter, also reflected in their share prices.

Source: Elara Research, Stocks/ sectors mentioned in this note do not constitute any research report/recommendation of the same and the Representative Portfolio may or may not have any future position. Past performance is not a reliable indicator of future results.

Overall, a decade later and having eaten a lot of humble pie – I do believe I made the right decision to sit on the flight back from London. Despite the market making all sorts of erratic moves in these years, my biggest learning has been this: that operating fundamentals do matter, even if only in the medium to long-term – and that one needs to stay alive first, to be able to play at that time. That’s the long and short of it.

{kind=link}

{kind=link}

Leave a comment