Have you ever marveled at the incredible strength of an airborne behemoth? A magical vehicle that can take you across the globe in hours? An invention humankind is most proud of, and powered by?

Yes, we are talking about an airplane. But how does a massive metal machine take to the skies, soaring with impeccable elegance? The secret lies not just in engineering but in the fascinating realm of metallurgy.

Could you retrace an entire airplane back to a single metal? If you’re thinking Aluminum, you’re on the right track.

When this simple element is combined with a few other elements that bring in their own unique characteristics, it all transforms into an indispensable part of aircraft design. This idea of transformation – the magic of combining diverse elements to produce something stronger and more resilient – finds an exciting parallel in the world of investments with Multi Asset Allocation (MAA) strategies.

The metallurgical marvel: Aluminum's metamorphosis

Aluminum is quite a soft and pliable metal. On its own, its applications are limited due to its innate characteristics. But introduce elements like copper or zinc into its structure, and voilà! You get an alloy that's not only stronger but also corrosion-resistant. This ‘revamped aluminum’ now becomes suitable for a plethora of applications, ranging from robust automobile parts to intricate aircraft components. It's a testament to the power of combination, where the resulting product is significantly superior to its individual constituents.

Synergy. Of the right kind.

Investment illusions: The diversification confusion

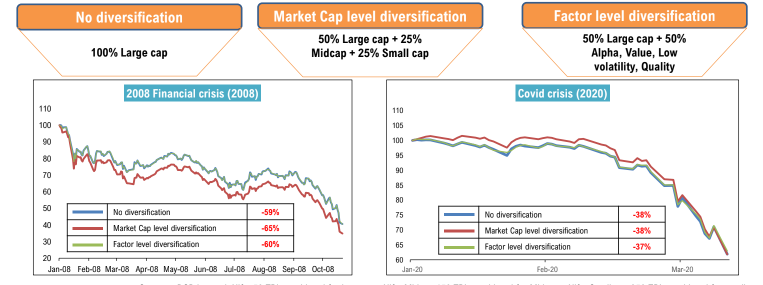

Now, let's transition from metals to investments. A prevalent belief in the investment community is that diversifying, even if within a single asset class, say equities, is a decent silver bullet against market uncertainties. This sentiment draws from the assumption that all assets in a category won't decline simultaneously. However, the turbulent waves of the 2008 financial crisis and the stormy winds of the COVID-19 downturn dispelled this myth. Diversification, as we've seen, requires a broader perspective.

Source – DSP Internal. Nifty 50 TRI iconsidered for large cap, Nifty Midcap 150 TRI considered for Midcaps, Nifty Small cap 250 TRI considered for small caps & Nifty alpha quality value low-volatility 30 TRI considered for factor diversification.

If you see the charts above, you’ll notice that during systemic equity market declines, you will need to consider much more than unidimensional diversification.

Do “defensive sectors” or multiple kinds of actively managed equity funds help with diversification?

In the ever-evolving realm of investments, there's an eternal quest to strike the right balance between risk and reward. As we navigate this journey, two tools often come up in the diversification toolkit: defensive sectors and active equity funds. But do they genuinely add value? Let's dissect each:

The defensive play

Defensive sectors, often referred to as non-cyclical sectors, include industries that tend to be more resistant to economic fluctuations. Think of utilities, healthcare, and consumer staples. People will always need electricity, medicine, and basic goods, regardless of the economic climate.

- Stability during storms: Defensive sectors can offer a semblance of stability during economic downturns. When cyclical sectors take a hit due to recessions, defensive sectors often remain relatively stable, cushioning the portfolio.

- Consistent returns: While they may not provide skyrocketing returns during bull markets, defensive sectors often yield consistent dividends and returns, making them an attractive component for conservative investors.

This is all in principle. However, in practice, things are seldom this straightforward. The truth is, when there is a systemic fall in equity markets, every sector (including defensives) experiences a drawdown.

.png?width=554&height=356&name=image%20(4).png)

Source – DSP Internal.

The ‘actively managed equities’ angle

Active equity funds, managed by seasoned professionals aiming to outperform the market, take a hands-on approach to stock selection.

- Potential for outperformance: With rigorous research and analysis, these funds might tap into high-performing stocks before they become mainstream picks, leading to potential market-beating returns.

- Tactical flexibility: Active managers can respond to changing market conditions, moving assets around to leverage opportunities or shield from impending risks.

However, similar to defensive sectors, even active equity funds are likely to experience a drawdown in case of systemic fall in equity markets. There’s no escaping this.

.png?width=396&height=374&name=image%20(5).png)

Source – DSP Internal.

Combining the steady nature of defensive sectors with the dynamic approach of active equity funds could indeed offer some semblance of diversification in theory, although it’s tricky. It's essential to remember that while they bring variety, they're not a panacea. The real test lies in how they interact with other assets in a portfolio at an overall level.

Why adding new funds might not always give you diversification benefits

The common adage "don't put all your eggs in one basket" is a cornerstone of investment wisdom. Naturally, one might assume that adding more funds to a portfolio automatically ensures diversification.

However, this isn't always the case. Here's why:

- Overlap of holdings: Two seemingly different equity funds might have significant overlaps in their stock selections. So even though you've added a "new" fund, you might just be increasing exposure to the same set of companies.

- Correlated performance: Just because funds have different names or are managed by different AMCs doesn't mean they respond differently to market conditions. Is your purported diversification merely superficial?

- Dilution of strategy: Every fund comes with its own strategy and focus. Continuously adding funds can dilute your own core strategy, leading to a rudderless portfolio that's spread too thin.

- Increased complexity: More funds mean more tracking and potential decision paralysis. At some point, the added complexity will start outweighing the benefits of perceived diversification. Law of diminishing marginal utility, remember?

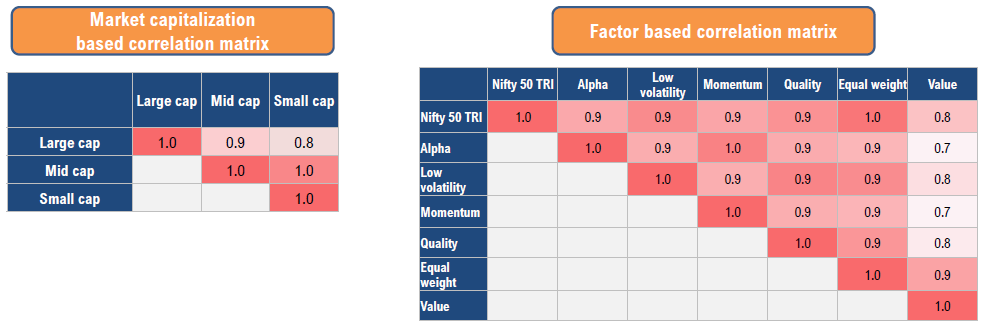

Source – DSP Internal, Data as on 31 Jul 2023. Nifty 50 TRI considered for large cap, Nifty Midcap 150 TRI considered for Midcaps, Nifty Small cap 250 TRI considered for small caps & Nifty alpha quality value low-volatility 30 TRI considered for factor diversification. NSE factor indices are used for factor-based correlation.

Ok, so how should one create a properly diversified portfolio?

Building a diversified portfolio is akin to constructing a sturdy building. Just as a strong edifice requires a mix of different materials, each serving its purpose, a robust portfolio needs a blend of diverse investments to stand firm against the vagaries of the market. One essential tool in this construction is understanding correlation, especially the power of low or negatively correlated assets. Let's delve deeper into the blueprint of a truly diversified portfolio:

The essence of ‘correlations’ while investing

Correlation is a statistical measure that describes how two assets move each other in relation to one other. A perfect positive correlation (a correlation coefficient of +1) means the assets move in exactly the same manner, whereas a perfect negative correlation (a coefficient of -1) implies that as one asset moves up, the other moves down.

- The power of low correlation: Assets with low correlation don’t move in perfect tandem. In the landscape of investments, this means when one asset class is experiencing a downturn, the other might remain stable or even appreciate, balancing out the overall portfolio.

- The counterweight of negative correlation: This is the gold standard for diversification. Including assets that have a negative correlation means they act as counterweights to each other. As one dips, the other rises, effectively hedging risks and adding stability to the portfolio.

Incorporating different asset classes

To harness the advantages of correlation in diversification, one must look beyond just one single asset class like equities. Here's why:

- Equities vs. bonds: Historically, equities and bonds have showcased low to negative correlation, especially during market downturns. When stock markets tumble, bonds, especially government bonds, often gain ground, acting as a cushion.

- Commodities and equities: Commodities, especially precious metals like gold, often move inversely to stocks. During economic uncertainties, investors flock to gold as a safe haven, making it an effective diversification tool.

- Global diversification: Expanding horizons beyond domestic markets by investing in international equities or bonds can reduce country-specific risks while giving your portfolio a different flavor.

- Real estate: Real estate investment trusts (REITs) or direct property investments can act as a hedge against both equity and bond market volatilities, given their unique set of influencing factors.

- Alternative investments: This might include assets like hedge funds, private equity, and even collectibles. Their performance doesn't typically align perfectly with mainstream asset classes, adding another layer of diversification.

Does this work? In short, yes.

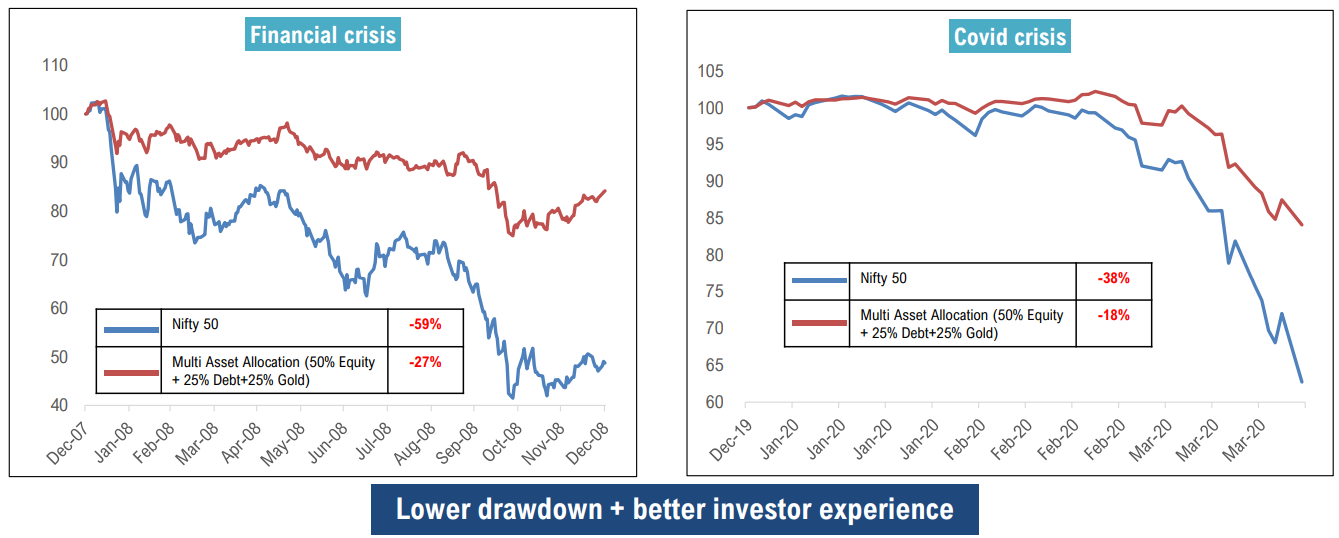

Here’s a look at the drawdowns (by how much the value of something falls) when asset classes like Gold and Debt are added to equities- track how the impact on the maroon line is lesser in times of crises:

Source – DSP Internal, Data as on 31 Jul 2023. Nifty 50 TRI, CRISIL Ultra Short Duration Debt B-I Index, XAU/INR considered for Indian Equities, Indian Debt & Gold respectively. Annual rebalancing considered.

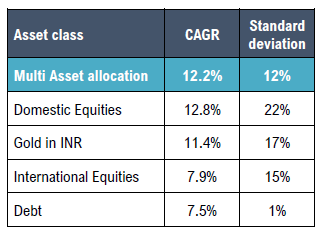

Further, see the amazing story the table below tells. Compare the returns below per asset class vs the standard deviation of each. Then look at the first row of the table again. A Multi Asset Allocation strategy back-tested for over two decades offered Equity-like returns, at almost half the volatility!

Nifty 50 TRI, CRISIL Ultra Short Duration Debt B-I Index, XAU/INR, MSCI ACWI TRI considered for Indian Equities, Indian Debt, Gold & International equities in ratio 50%,15%,20%,15% respectively for the Multi-Asset portfolio mentioned above.

And its easy to understand why a thoughtful mix has worked better, when you consider that in the 23 years since the Year 2000, Equities have been the best performing asset class only 10 times, while Gold has been on top in 7 years, Debt in 4 years and International Equities in 3 years (including YTD 2023)!

Is this the right time to consider a Multi Asset Allocation strategy?

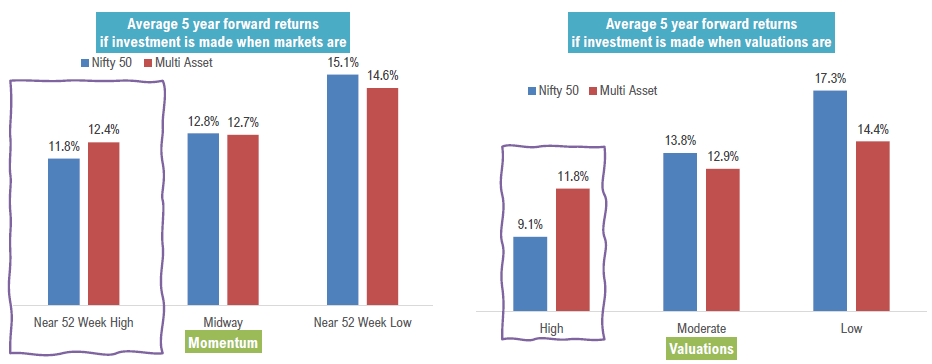

We are writing this blog in Aug 2023. Today, two key realities worth underlining are that equity markets are hitting highs, while valuations are nearing peaks (if not already hitting peaks).

In times like these from the past, what strategy has ended up doing better over the next 5 years? See the two charts below and the answer will jump out at you.

Data from 01 Jan 2004 to 31 Jul 2023. 10% buffer is considered for determining whether markets are near 52 week high/low. P/E & P/B of Nifty 50 is considered to determine if valuations are high/moderate/low. Nifty 50 TRI, CRISIL Ultra Short Duration Debt B-I Index, XAU/INR, MSCI ACWI TRI considered for Indian Equities, Indian Debt, Gold & International equities in ratio 50%, 15%, 20%, 15% respectively for the Multi asset portfolio.

Diversify to Strengthen: The Multi Asset Allocation approach

The case for Multi Asset Allocation Funds, the financial equivalent of our alloyed aluminum, has is now quite strong, if you’ve gone through the evidence above. To summarize:

- Act as a shield against fluctuations: Just as diverse elements provide strength to Aluminum; different asset classes offer a protective barrier against the fickle nature of domestic or global events.

- Help you tap into diversity, correctly: A correctly diversified portfolio by its very nature won’t always be the best performer. But in times when things aren’t looking good, the different elements will play their part to reduce the impact of fluctuations, thereby helping you survive better, and for much longer.

- Dynamic portfolio management: With a pulse on domestic and global trends, a good strategy manager will recalibrate and shuffle assets, ensuring that the investment mix remains optimal, much like a metallurgist refining an alloy formula depending on evolving needs.

- Taxation: There is clear tax efficiency embedded in the very structure of a multi asset allocation strategy, when run as a mutual fund. Unlike individual investors who face tax impact each time they buy, sell stocks or funds or rebalance their portfolios, these funds can recalibrate allocation without triggering tax liabilities for investors.

In essence, the Multi Asset Allocation strategy can be like the alchemist's potion in the investment realm. By artfully mixing diverse elements, it strengthens the core, offering relevant resilience against downturns while also offering sound potential for appreciable growth.

Invoking “MAA”

Right at the beginning of the blog, we abbreviated Multi Asset Allocation to MAA. This was a thoughtful choice, not just a happy coincidence.

Just like your mom is always there to take care of you, this strategy’s very aim is to make your investing journey smoother and keep your long-term game on point.

Which is why we say, #JustLikeMAA

Leave a comment