-1.png)

The Indian stock market, like its many counterparts around the world, can be carved up into baskets of stocks using several different criteria, with the most common two being market capitalization and revenue. However, another useful way of segmenting the market is by sector or industry. Seen this way, the market can be broken up into multiple sectors such as pharma, IT, infrastructure, energy, automobiles, or banking.

It is this last sector that is of interest to us today, as we believe it’s currently looking poised to deliver reasonably solid performance over the long term.

Let’s see why this is so, and how retail investors can best capitalise on its potential growth.

Banking: on the Uptick

As a result of the growing middle class, greater disposable incomes, and the digitalisation of various processes, several Indian banks have seen excellent growth during the past decade. For instance, during the 10-year period from 2009 to 2019, HDFC Bank delivered a whopping 668% return.

There are several reasons why the overall banking sector looks attractive right now. Here are just a few of them:

-

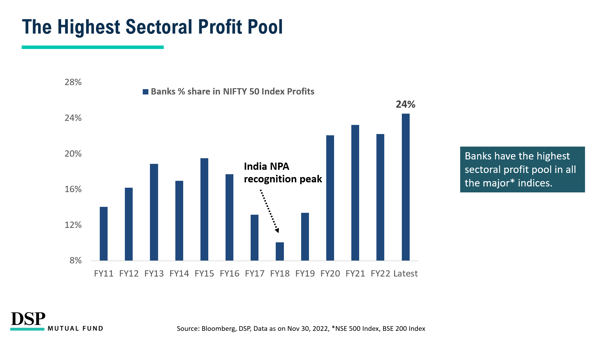

The highest sectoral profit pool

As of November 2022, banks have the highest sectoral profit pool in two key market indices, namely the NSE 500 and the BSE 200. And the banking sector’s share of the Nifty 50’s profits was an impressive 24%.

-

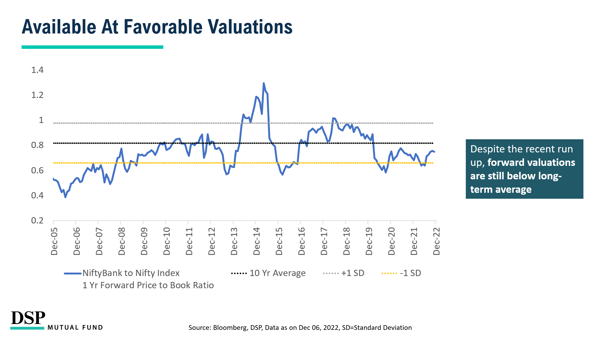

Available at favourable valuations

Despite the recent spikes in several bank stocks, the forward valuations of the stocks in the banking sector as compared to the market are still lower than their long-term (10-year) average.

This effectively means that the banking sector is very attractively priced right now, relative to its performance.

-

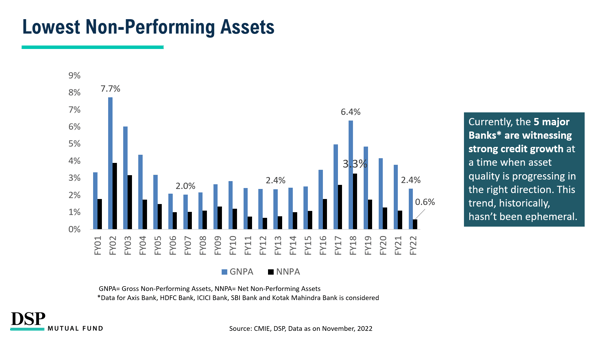

Lowest non-performing assets

Non-performing assets (NPAs) in five of the biggest Indian banks have been on a downward trajectory ever since a spike in FY18. Indeed, not only is asset quality improving, but these banks are also seeing strong credit growth. Historically, such trends have typically not been short-lived.

-

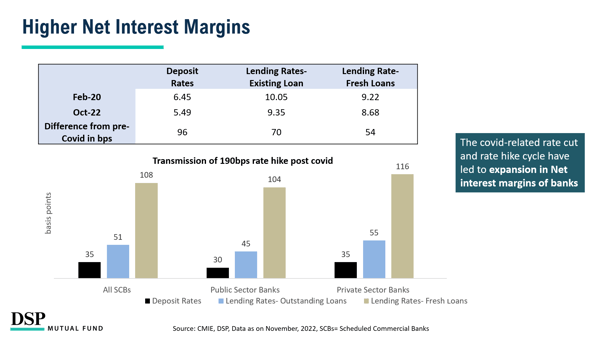

Higher net interest margins

The Covid pandemic triggered several interest rate cuts and hikes in the past two years. An important consequence of these cycles has been that banks now find themselves with higher net interest margins.

-

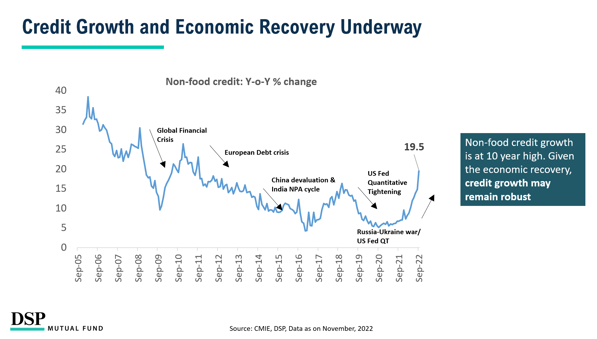

Credit growth and economic recovery are underway

The slump in credit and general economic activity in the wake of the Covid pandemic has given way to robust credit growth and a strong economic recovery. Indeed, non-food credit is currently at a 10-year high, which is excellent for banks, particularly if it can be sustained by further economic growth.

-

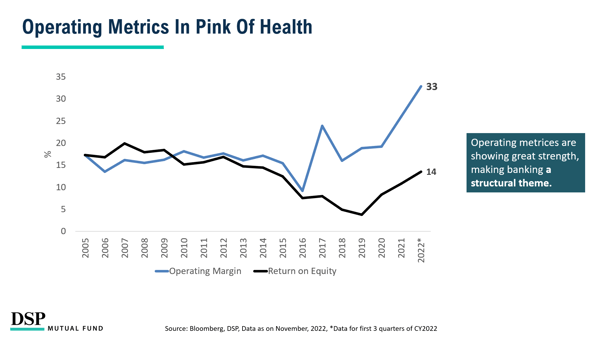

Operating metrics in excellent shape

Various key operating metrics for banks have seen dramatic growth since 2020, including operating margins and return on equities.

All these factors seem to suggest that now is an excellent time for retail investors to seriously consider taking exposure to the banking sector.

A convenient way to do so would be to buy units of a fund that tracks/ replicates a banking-specific index. Let’s quickly understand what this means, and then take a closer look at the Nifty Bank Index.

Nifty Bank Index: the index of choice for banking?

We have discussed a sector-oriented approach to investing before. Investing in a specific sector can be made easier through a fund that aims to mimic or “track” a sectoral index — typically an index fund or an exchange-traded fund. An index fund is a fund that aims to mimic an underlying index exactly. For example, if Rs. 1 lakh is invested in a Nifty 50 Index Fund, it represents investments in all the 50 stocks of Nifty 50 in a proportion represented by each stock’s weightage. The aim of an index fund is to generate returns similar to its benchmark index.

One of the most important Indian indexes for the banking sector is Nifty Bank, which reflects the performance of the largest (by market cap) and most liquid banking stocks in India.

Several key factors make Nifty Bank a worthy index to track:

-

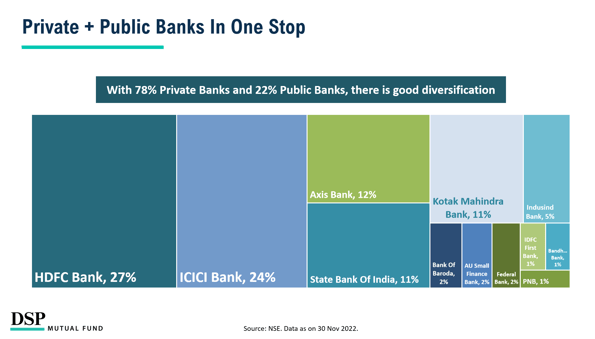

Diversification

78% of Nifty Bank Index is made of private banks, with the rest being public banks, which represents a reasonable degree of diversification.

-

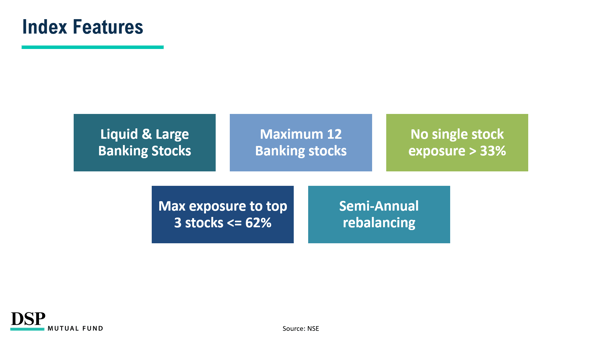

Well-picked criteria

Nifty Bank is subject to several criteria that serve to maximise its value as a barometer of the overall banking sector. For instance, no single stock can represent more than 33% of its value, and only large and liquid stocks are eligible to be a part of it.

-

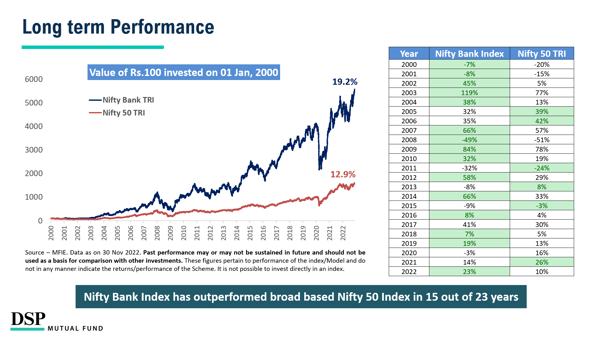

Excellent long-term performance

Nifty Bank has outperformed the broader Nifty 50 index in 15 of the last 23 years. Moreover, if one were to look at the 10-year rolling returns, Nifty Bank has outperformed Nifty 50 98% of the time!

While all of these factors certainly make banking look like a must-invest sector, it should be noted that any fund that tracks Nifty Bank Index will be subject to certain specific risks, including:

- Concentration risk, since Nifty Bank only consists of 12 stocks

- Relatively high volatility compared to diversified equity funds

- The chance of underperformance when compared to diversified equity funds

Give the banking sector some credit!

Thus, when all is said and done, the banking sector is likely to make for a good addition to your portfolio and could potentially deliver highly satisfactory returns over the medium and long term. Indeed, India might become the third-largest domestic banking sector by 2050, and investing in this sector now could be a smart way to capture a lot of the value that is likely to be generated during that journey.

How can you bank on India’s growth? Check out this brand new offering that can help enable this for you.

Leave a comment