The reality of stellar IPO returns in the past

Let’s step back to the year 2007. The markets were having a good time and real estate stocks were soaring like there is no tomorrow. It was such an opportune moment that DLF (erstwhile DLF Universal) decided to go public by launching their IPO. The over Rs 9,187 crore IPO saw subscription 3.5 times that was enough to push the price up nearly 36% in debut trade on July 5, 2007 upon listing. It closed the day up 8%. Within a few months’ time, promoter KP Singh had joined the creme-de-la-creme as the richest Indian billionaire, second only to Mukesh Ambani.

Year 2008 saw participants flock to the markets to get a piece of the Ambani-led Reliance Power that debuted at the stock exchange with a Rs 11,560 crore IPO. The issue attracted over 5 million bids and was oversubscribed nearly 70 times the offer. But guess what? The stock slumped 17% on its first day, on February 11, 2008- much to the anguish of retail participants who were offered a mere Rs 20 discount.

What stories like these and many more gave rise to, is an investing strategy called the IPO investing strategy. Some ‘investors’ (and I’m using the term loosely here) invest only for the listing gains that IPOs may offer, while others enter the markets only through IPOs.

Well, to be fair, some IPOs, especially ones from the dotcom bubble era have returned manifold over time. However, stellar returns from IPOs are a reality only for those who have the experience, the foresight and the willpower to exit at what seems like ‘the right time’. After all, other IPOs that offered high initial listing gains eventually failed to offer long-term, sustainable returns.

The risk associated with IPO investments

The year 2021 saw a significant increase in IPO volume and proceeds globally. According to the EY Global IPO Trends Report, the global volumes and proceeds in 2021 were 60% higher than in 2020. Back home, India’s investor population has exploded by an additional 15 million since the pandemic, after stagnating at about 20 million investors for decades. A release by the National Stock Exchange (NSE) says that 5.13 million investors were added in just four months—1 April, 2021 to 25 July, 2021.

And IPOs ruled the roost in 2021. Of the total 65 IPOs launched in the year, 17 had an issue size of over Rs 2,000 crore and eight had an issue size of over Rs 5,000 crore. 45 of them gave positive returns while 20 sadly burned wealth as of December 30, 2021.

This brings to light the fact that participating in IPOs is risky. It isn’t a guarantee of wealth multiplication ever, as many people seem to have convinced themselves. Investors need to research well about the company’s background, associated parties, and other aspects before investing. They must also be aware of their own risk appetite and not put everything at stake in the expectation of magnificent returns. Risk hai, hamesha rahega.

Recently, the news of LIC’s IPO has sent ripples across the market. Both seasoned and new investors alike are saving up, expecting to get an allotment, betting on listing gains and a good future. However, note that the retail share of the public offer is set at 35%. This means a sizeable chunk of excited investors will be left disappointed.

This brings us to the question - does an IPO investing strategy work for retail investors? For simple people like you and me- middle class, salaried individuals with big life struggles that make investing well seem like a low priority item on our agenda? Couldn’t it have been more profitable to invest that same money in another, more known investment and reap returns rather than waiting?

Many argue that it is just luck and the listing gains, if offered an allotment, will make up for the uncertainty. Risk ke aage returns hai, they say. While that may be true for some companies, many other IPOs do not perform as expected. India’s biggest IPO till date - Paytm - is a case in point.

Although the Rs 18,300 crore Paytm IPO was oversubscribed by 1.8 times, the share price fell by over 27% on the listing day. This led to a wipeout of nearly 25% of investor wealth amounting to Rs 39,000 crore on the listing day itself. The stock has since tanked more than 70% (from listing price) as of March 31, 2022.

Kalyan Jewellers India Limited, Windlas Biotech and CarTrade are some other sad IPO stories in 2021 that have been eroding wealth for investors since listing.

Risks in IPO investing strategies stem from limited quotas reserved for retail investors, unrealistic valuations based on (what seems like obscene) liquidity offered by venture capitalists, the absence of adequate data to assess future performance, investor bias and the perception games, and the inability of investors to make realistic and honest predictive analysis.

The truth is, retail investors are often intrigued by the media hype around an IPO. Various factors affect growth and many of them are not even in the company’s control. While an IPO may be critical for any business for various reasons, going simply by media hype to hunt for an ‘early investor’ advantage is one of the many mistakes that retail investors make.

Remember, at the heart of it, all investing strategies are based on the same basic tenets- good businesses, run by good people, available at good prices. Deciding to invest during an IPO should be no different.

The no rocket science alternative:

Investing in mutual funds could be a great alternative for retail investors instead of going for an IPO investing strategy. They are a more effective way to manage risk because mutual funds are managed by professional fund managers who analyze deeply and keep a close watch on multiple businesses, track their performance, study their potential, meet the people that run these businesses often to get insights that you and I may not be able to find, unless we are the next Warren Buffett or Charlie Munger. It is the fund manager's job to create a portfolio of different high-potential businesses so that the overall risk gets reduced, you get the potential for wealth creation and sensible returns, and you don’t need to do the hard work and place bets on many individual companies.

If you still insist on putting money in IPOs but don’t want to run the risk of putting your money in only one company’s IPO (running a high risk), you could also consider MF based options that invest in multiple IPOs and aim to fetch you similar or greater returns at potentially lower risk. The fund managers research extensively to come up with the right IPOs to buy. They try to not fall prey to the hype and excitement around every IPO that shows up on the radar, unlike us regular folk. There is atleast one such fund that I’m aware of, but you’ve got to do your own research to figure out which one (it is competition after all 😊).

Mutual funds also ensure that your money starts yielding a return immediately instead of waiting for the lottery of IPO allotment. And then many investors, even those with deep pockets (remember this recent Shark hullabaloo that happened?) don’t even get units allotted despite the waiting and the excitement- forget the returns! Since mutual funds put your money to work immediately and also diversify investments across multiple companies, you won’t be putting all your eggs in one basket- thus, mitigating the risk of losing all or a big part of your investment at once. Mutual funds are simple instruments, and allow you to invest small or big amounts or opt for systematic investment plans rather than investing only a lump sum, like IPOs seek. See where I’m going?

If you need some evidence that even a basic investment strategy in broad-based MFs works, check this out…

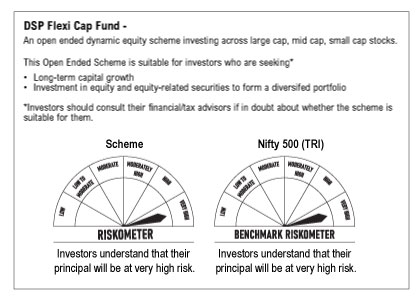

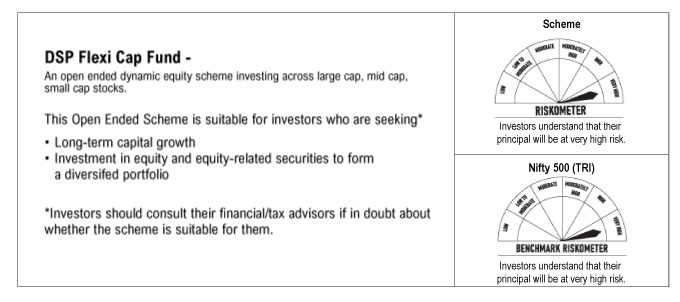

An investment in DSP’s oldest equity fund DSP Flexi Cap Fund, at inception in April 1997 has risen 78 times (19% each year, on average) over approx 25 years (till Mar 31, 2022). And had you invested just Rs 5,000 every month via a SIP since inception in DSP Flexi Cap Fund, your approx Rs 15 lakh cumulative invested amount would have grown to a massive Rs 2.4cr+. This is a whopping absolute growth of over 1500% and an annual average growth of 18.7%!

Not bad for what seems like plain vanilla investing, vs fancy but dangerous IPO investing strategies, right?

This is not to say mutual funds don’t involve risks. No investment is risk-proof- even DSP Flexi Cap Fund’s lowest ever return over any 1 year period was -54%, while the highest ever 1 year return was 154%- goes to show that in really short periods of time, even in MFs, anything can happen. However, with mutual funds, your exposure to risk is minimized or managed by professionals since you invest in multiple businesses, not just one- which means you can invest in peace instead of being jumpy about your single exciting IPO investment- often a black hole in many ways!

So, what would you like to do? Chase the fancy IPO mirage or invest in an awesome, no-rocket-science alternative?

Leave a comment