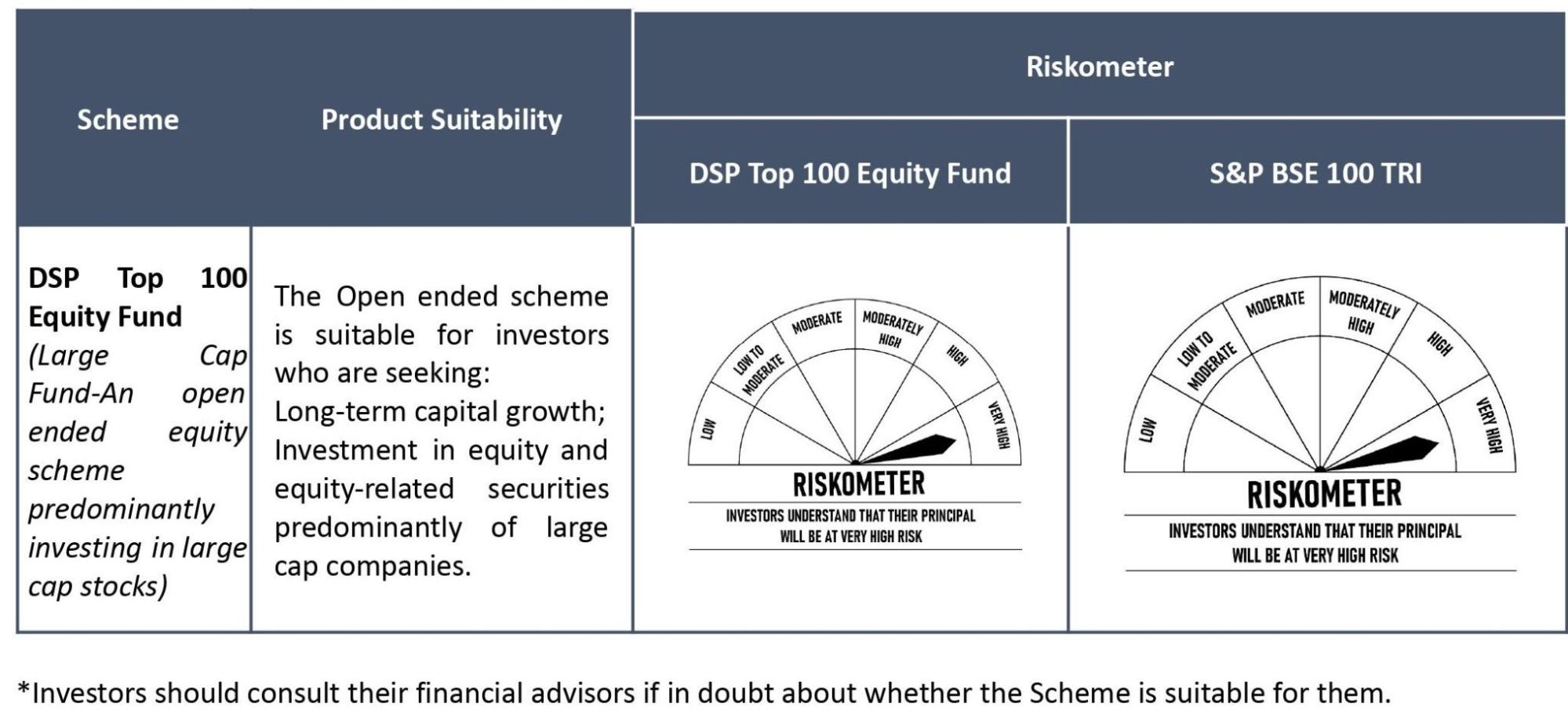

| I have been managing DSP Top 100 Equity independently since 1st September 2022. In my mind, I am addressing my first letter to my younger sister who has recently invested in the fund. She is probably amongst my least sophisticated investors. For any feedback or queries regarding the portfolio feel free to write to DSPTop100@dspim.com |

Dear Investor,

Thank you for investing in the DSP Top 100 Equity Fund. Let me tell you about the implications of this decision.

Perhaps you have come across Yoann Bourgeois’ routine on the stairway and trampoline. It is a mesmerising act of grit and grace. It is a visual metaphor for life - a reminder of the delicate balance between security and instability and the importance of finding equilibrium in an unpredictable world. Investing, Equity investing in particular – is similar. Just as Yoann Bourgeois must navigate the rigid structure of the staircase and the volatility of the trampoline, investors must find balance between stability of their approach and fickleness of markets.

Equities (or Stocks) as an asset class, over the long term, have often comfortably beaten inflation. They have the potential to generate relatively higher returns than debt investments (like your fixed deposits for example*). Equities are liquid - you can buy/sell relatively easily, well-regulated and tax efficient in India.

The most popular benchmark for Equity market performance in India is the NSE Nifty 50 Index. It is like a score for how well big companies are doing. The score is calculated by giving certain weights to the fifty biggest companies in the country in terms of their market value. If the stocks of these companies are doing well, the score goes up, and if they are not doing well, the score goes down. Occasionally some companies in the Index get replaced by other companies that are doing relatively better.

Investors often want to know how much money they can make, potentially, by investing in Equity. While returns can vary depending upon a lot of factors, let me share a broad framework about how to think about this.

*The comparison with PPF, Bank Fixed Deposit (and other traditional saving instruments) has been given for the purpose of the general information only. Investments in mutual funds should not be construed as a promise, guarantee on or a forecast of any minimum returns. Unlike traditional saving instruments there is no capital protection guarantee or assurance of any return in mutual fund investment. Traditional savings instruments are comparatively low risk products and are backed by the Government (except 5- year recurring deposits). Investment in mutual funds carries high risk as compared to the traditional saving instruments and any investment decision needs to be taken only after consulting the Tax Consultant or Financial Advisor.

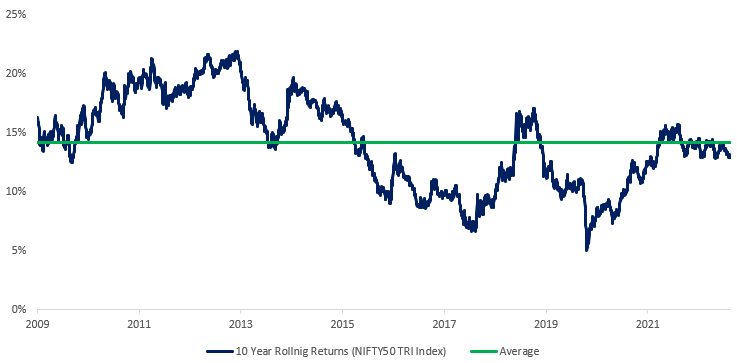

First you need to be patient when investing in stocks. It’s better to think in terms of decades, not just months or a few years. Over 10 year rolling periods Nifty 50 index has delivered on average about 14% CAGR# (compound annual growth rate) returns. This is assuming dividends are also reinvested (for this we use something called “Total Returns Index” or “TRI”). 63% of the time the returns are between 12% to 20%. As we will discuss later, participation in any Index, in any form, also incurs some cost.

I like to think of Equity in India as a 12% -15% return asset on average. Your actual returns could be higher or lower, but this range is a rational “return expectation”.

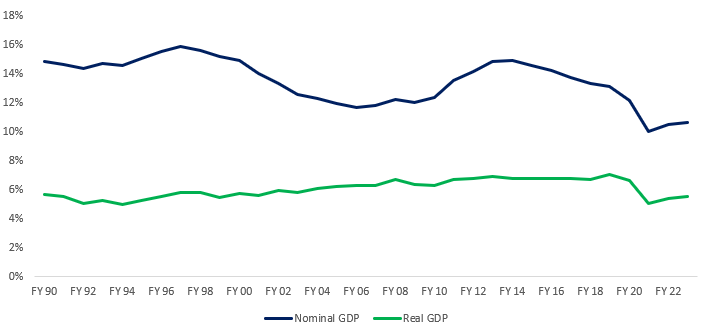

Another reason why a 12% - 15% number is reasonable is because it's about the same as the growth of the Indian economy. The Indian economy has grown by about 5.8% (real GDP) on average since 1990 and prices have gone up by 7% (inflation) on average annually. This leads to an average nominal growth of about 12.8%. Real GDP corresponds to volume of activity in the economy while Nominal GDP also takes into account the rising prices of products and services. The aggregate profits and hence value of companies in the country also track this number. Larger established companies often also end up taking some share from smaller, unorganised players in the economy.

Nifty 50 TRI Index

Source: Bloomberg, Internal

Source: Bloomberg, Internal

# Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. These figures pertain to performance of the index/Model and do not in any manner indicate the returns/performance of the Scheme. It is not possible to invest directly in an index.

India GDP Growth (10 year rolling)

Source: NSO, Internal

Source: NSO, Internal

If you invest in a crash or when the markets are not doing well (when newspaper headlines are scary) you might make more than 15%. And if you invest when the market is roaring (when people around you claim to be getting rich ‘trading’ the market) the returns could be lower than 12%.

Before you scoff at a 12% CAGR returns please note that at this rate you more than triple your investment in 10 years and more than 10X in 21 years. As I said: think decades not years.

Imagine you could invest in a special kind of savings account that pays 14% interest each year (“imagine”). And at the end of every year, you pay 20% of the gains in taxes. At 10% long term equity capital gains taxation, this savings account with a phenomenal yield of 14% ends up making less than Equity yielding 12% CAGR. If you pay 30% in taxes, then this savings deposit will have to offer more than 17% yearly interest to match Equity returns over 10 years. This is what I mean when I say Equity is “tax efficient”.

I am sure you have come across many opportunities that promise quick riches, with returns that are much higher than 12%-15% that a rational investor should expect from Equity on average over the long term. But, please be aware that these opportunities often come with risks that are not immediately obvious and that a lot of people who invest in them do not fully understand.

Most investors will do well with Equities as the core of their investment portfolios.

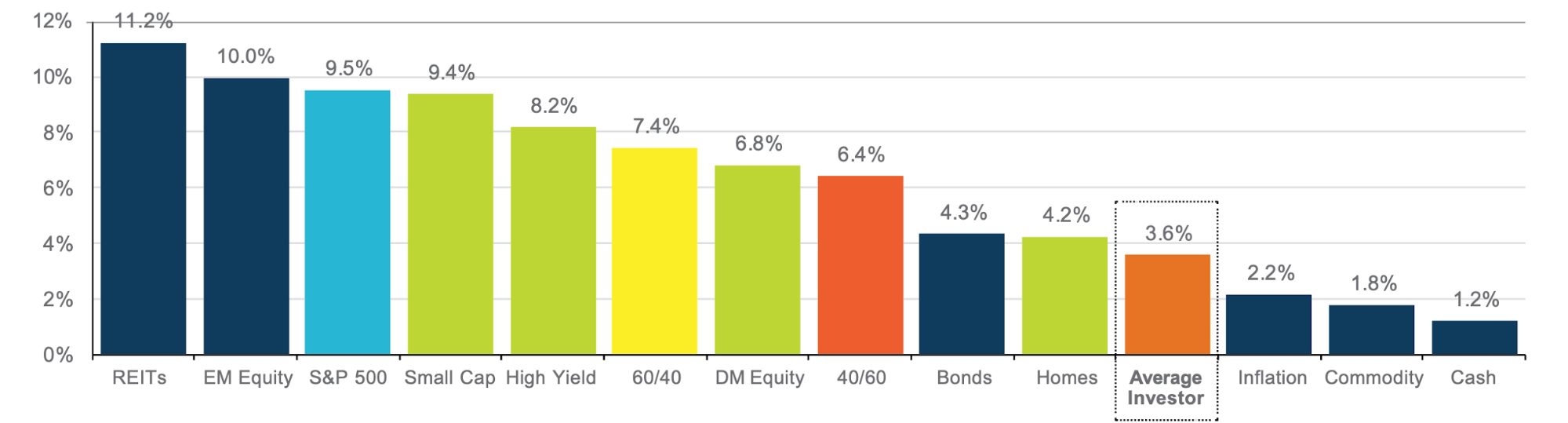

Given the historical returns one would assume than an average investor would be beating inflation handsomely over time. Unfortunately, that is not correct.

In fact, over the last 20 years, the average American investor has earned only 1.4% more than inflation. That's not very much. Even a conservative mix of stocks and bonds (a 40:60 Equity: Debt portfolio) earned 2.8% more than the average investor over the last 20 years. This is likely due to pro-cyclical behaviour, where investors tend to chase the best performing styles, funds or asset classes and exit them when they are underperforming. Instead of buying low and selling high we have a persistent tendency of doing the opposite. Investors are basically timing the funds, the asset classes, and styles poorly.

Instead of trying to figure out when to buy and sell different investments, or looking for the next big thing, it is better to be patient and stick to a sound plan over time.

Any plan, fund or strategy that allows you stay invested longer can significantly improve your investing outcomes by reducing mistakes, costs and tax out flows.

20 year annualized returns by asset class ( 2002-2021)

Source: JP Morgan, GTM Report

Source: JP Morgan, GTM Report

What does it mean to own a stock or an Equity fund?

When you buy a stock, you pay the current market price for the shares and become a shareholder in the underlying company. The number of shares you own represents your proportional ownership of the company relative to the total number of outstanding shares.

What that means is: investing in equities empowers even those with limited savings like us to become co-owners of some of the world's most successful and profitable companies. It's nothing short of magical.

In about 15 years, India's population is projected to exceed China's and become more than the World population in 1900. With the second largest labour force globally and projected to grow for the next two decades, there is significant potential for Indian businesses to increase their earnings and market values.

How do you participate in this growth?

You can invest in an "Index" fund (Indexing) which in turn buys a bundle of stocks that are similar to the ones in a big stock market index like Nifty 50 Index. The people who manage the fund, called fund managers, don't get to pick and choose which stocks to buy. They just make sure the fund has the same stocks as the Index. This is often a simple and low-cost way to invest in stocks. Your actual returns may be slightly lower than the Index, usually between 0.3% to 0.7% per year, due to costs and something called "tracking error".

Index funds are passive funds because the fund managers do not actively pick the stocks that go into the portfolio. They simply replicate the underlying index. On the other hand in active funds like DSP Top 100 Equity Fund, the fund managers, like me, try to pick a portfolio with the objective of doing better than the Index.

Active funds over time have struggled to beat the underlying Indexes (their “benchmarks”). This problem has been particularly acute in the Large Cap category which DSP Top 100 Equity Fund is a part of.

The degree by which an active fund outperforms its underlying benchmark is referred to as “Alpha”. Unfortunately, the alpha in the large cap category has been negative, meaning that many active funds have not only failed to outperform the benchmark Index, but have underperformed it.

Some reasons that are proposed for the lack of alpha (some analytical jujitsu here, frequently debated, often useless, feel free to skip this section):

It is a negative sum game: What it means is that if I make more than the Index somebody else must make less as in aggregate, we are the market. And as most active funds charge often close to 1.75% to 2% in expenses (in their regular schemes), this drag makes it a negative sum game instead of a zero-sum game.

In the small cap category, a majority of funds do have alpha. Where is this alpha coming from? In the 1990s and 2000s, funds in the large cap category also had alpha. Where did that come from?

About 50% of the Equity market is owned by promoters. They cannot diversify as widely as people like us. Their fortunes are often linked to the fortunes of a handful of businesses. They can and have been providers of alpha at times. There are a lot of inferior quality businesses that sometimes do get included in the Indexes due to temporarily favourable environments. Avoiding these have been another source of alpha in the past.

Too many smart people are trying to outwit each other. It’s too competitive: There are a lot of endeavours where the competition is high. Think about sports for example. Why do some teams and some players consistently beat others and have long unbeaten streaks? Is cricket or football any less competitive than investing?

Markets are just too efficient: Enough ink has been spilled here by people smarter and more eloquent than me. There are multiple interpretations of this efficiency. Look at stock prices of some of the most popular businesses on the planet. Can the underlying value of the business be so volatile? The price that the business is quoting at is almost always wrong. We often just don’t know whether it is too low or too high. I am not a believer of the standard efficient market hypothesis.

Then why are active funds underperforming Indexes?

At least in the large cap category few are even trying to beat the Indexes. To get better results than the Index (at least 2% better so that you cover your costs) you must 1. Hold a portfolio that is different from the Index 2. Be right. This first is represented by Active Share – a measure of how different your portfolio is from your benchmark. In the large cap category a majority of funds have active shares in the 30s and 40s (percent). This is too low.

The second and the more crucial part is being “right”. Now it’s almost impossible to judge how a business or a stock will do over a few quarters. But all the debate in our industry (internally, with channels, with distributors and end investors) is often about one-year horizons. Any negative deviation in performance is red flagged and analysed to death. There is constant feedback to fund managers to generate “smooth alpha”. The end result is, over time, everybody starts moving towards the Index. They become what in the industry is called “closet indexers”.

Smooth alpha is a myth. Bernie Madoff had smooth alpha.

The DSP Top 100 Equity Fund runs one of the most concentrated portfolios (low 30s stock count) with an active share of often 60% or more. What this implies is that in any month there is a 50% probability that the deviation in performance with respect to the Index can be 1.5% on either side. If the Index is flat the fund has a 50% chance of being 1.5% or higher or -1.5% or lower.

The investors I seek for this fund are ones who are not focusing on monthly or quarterly performance. Monthly and quarterly deviations are an inescapable cost of any potential alpha this fund might generate over time.

Most investors will do well with Index funds. If for no other reason than the fact that they would own that choice and stick to it when markets become volatile or crash – as they invariably will at some point. I have never invested in an Index fund but at the same time I never discourage anyone from doing so.

Incrementally if you want to invest in the Large Cap category in an active fund that runs a benchmark agnostic, high active share, relatively concentrated, value focused portfolio – then DSP Top 100 Equity Fund can be part of your consideration set.

Unfortunately, it can only be determined over time (retroactively) if an active fund manager's strategy and process were sound and effective. I hope over time numbers validate this for the DSP Top 100 Equity Fund. This is my mountain to scale.

This letter is just the beginning of hopefully a long conversation. In my next letter I will explain the portfolio construction approach of your fund and talk about some of the businesses you own through this investment.

We are grateful for the trust you continue to repose in us.

Regards,

Abhishek

January 2023

Amended as on Apr 1, 2023: Please note that as per amendments in Finance Bill 2023, from April 1, 2023, profits made on investments in debt mutual funds are now taxed as short-term capital gains if these funds invest <=35% in equities. This means debt mutual funds are now taxed as per the income tax rates as per an individual’s income.

Also note that with effect from Apr 1, 2020, Dividend Distribution Tax (DDT) was abolished, and mutual fund dividends were made taxable in the hands of investors. Dividend income is now considered as ‘income from other sources and investors need to pay tax on it as per their individual tax slabs.

This video was originally created at a time when tax rules were different. Please treat this note as the latest updated tax information.

Leave a comment