Welcome to the March 2024 edition of Netra, where we present data-driven market insights that can inform your investing decisions.

This month, we’ll talk about the shrinking risk premium associated with equities, the concentration risk currently faced by the tech sector, and the implications of slowing wage growth in India.

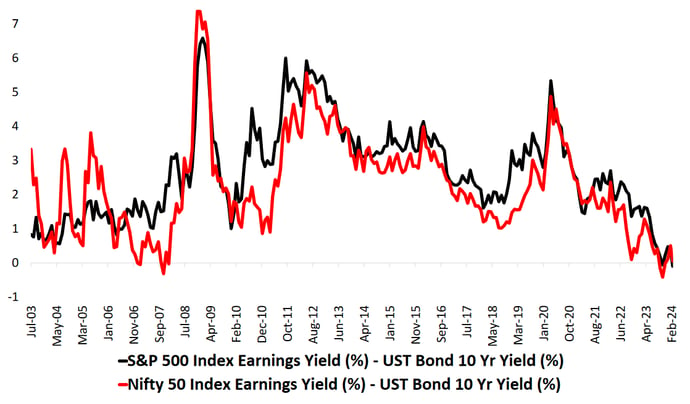

Are stock investors getting complacent?

Equities are typically more volatile and risky than government bonds, which is why stock market investors expect to receive excess returns for investing in stocks rather than bonds. This expected premium, aptly called the equity risk premium (ERP), serves to compensate equity investors for taking on additional risk.

One way to capture the ERP is by looking at the difference between the earnings yields of stocks and bond yields. Calculated this way, it turns out that the ERP is currently lower than it has been in more than a decade. In fact, the last time the ERP was this low was during the market euphoria that just preceded the global financial crisis of 2008.

Source: Bloomberg, DSP; Data as of Feb 2024

What does this mean? Well, one factor that affects the ERP is the perceived level of market risk. When the perceived risk is low, investors are willing to accept a lower premium for investing in equities, which exerts a downward pressure on the ERP, and vice versa.

So the unusually low ERP levels being seen right now likely correspond to a low perceived level of risk in the stock market. But here’s the thing: there is often a mismatch between actual risk and perceived risk (as was seen prior to the 2008 crash). In addition, a lower perceived level of risk can, ironically, increase the actual level of risk, simply because the perception of lower risk makes investors more complacent.

Thus, while the current ERP levels might not be indicative of anything catastrophic, they might be a sign of a general complacency and disregard for risk, which might make lacklustre returns more likely.

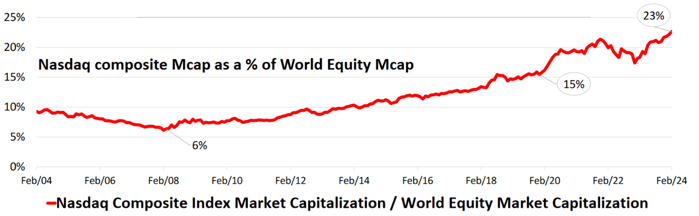

The flip side of tech’s phenomenal growth: high concentration risk

Most major equity markets bounced back strongly after plummeting due to COVID in 2020. However, it’s now clear that the tech sector in particular has outshone most of the others, so much so that it now carries a hefty concentration risk.

The market cap of the Nasdaq Composite Index (which is often considered to be a stand-in for the tech sector) now represents nearly a quarter (23%) of the global equity market’s capitalisation.

Source: Bloomberg, DSP; Data as of Feb 2024

If we were to add the contributions of tech companies in China, India, the EU, and the rest of the world, the tech sector’s global share in terms of market cap goes up to nearly 40%.

No individual sector has reached such heights before. The closest a sector last came to having such a massive influence on the markets was probably in the 1980s: approximations from past data indicate that the broad energy sector might have accounted for close to a third of the global equity market’s capitalisation at some point in that decade.

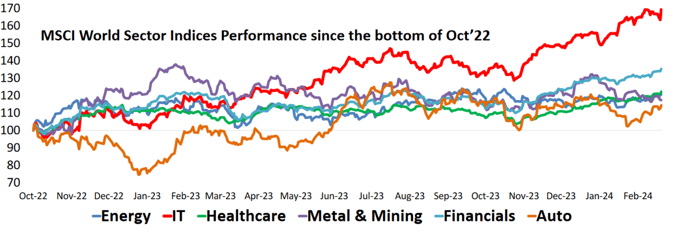

Moreover, while the IT sector has seen excellent growth over the last 18 months, the performance of most other sectors has been relatively unimpressive.

Source: Bloomberg, DSP; Data as of Feb 2024

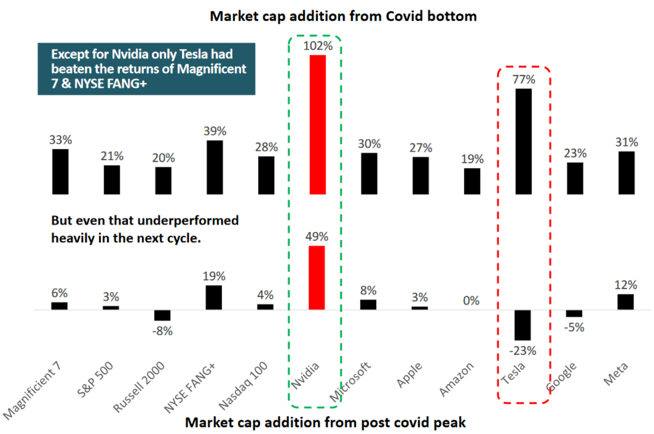

In fact, broadly speaking, only the semiconductor space and AI-related stocks have performed unusually well since November 2021. Currently, Nvidia accounts for the bulk of the returns (from the COVID bottom) of the NYSE FANG+ and Magnificent 7 cohorts, with Tesla being the second-biggest contributor. The broader market, including tech stocks, has been more subdued.

Source: Bloomberg; Data as of Feb 2024. Post covid peak here is taken as Nov 2021

In the words of entrepreneur and author Bob Farrell:

“Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.”

Thus, the dependence of the ongoing tech rally on a handful of names could be a sign of unsustainability. Investors in the sector would do well to be cautious.

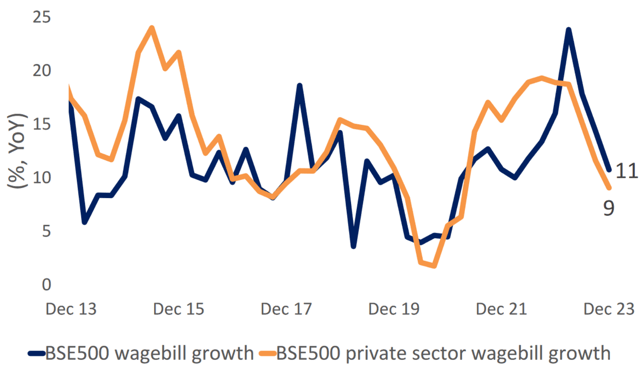

Slowing wage bill growth might bode ill for non-large-caps

The term ‘wage bill’ refers to the total amount paid by an organisation to its employees over some specified period. A few quarters ago, the overall wage bill growth of BSE500 companies stood at 20% YoY; it has now declined to 11% YoY.

Of particular concern is the fall in the wage bill growth of private sector companies, which now stands at 9% YoY: this is a ten-year low if the impact of Covid is excluded.

Source: Capitalline, Nuvama; Data as on Feb 2024

This slowdown in wage bill growth could negatively impact small- and mid-cap (SMID) stocks. Why? Well, many SMID stocks have done well in the recent past due to their excellent profit growth, which was largely driven by significantly higher margins. But if you add the slowdown in wage bill growth to subdued core inflation and the expectations of low nominal GDP growth, then the ability of SMID companies to maintain their performance and justify their valuations gets called into question.

The bottom line

Stock market investors might currently be disregarding the actual levels of risk, which could result in disappointing near-term returns. In addition, the high-flying performance of the US tech sector might make that space look tempting, but investors need to be mindful and circumspect, given the associated concentration risk. Lastly, Indian SMID stocks could face some headwinds in the near future.

For more actionable insights backed by data and analyses, we invite you to read the latest edition of Netra in its entirety.

Leave a comment